that makes tactical asset allocation decisions between cash, duration, and higher yielding investments to produce returns in both rising and sliding bond yield environments.. The strategy aims to outperform the Benchmark in terms of net total return over rolling three-year periods by investing primarily in Australian fixed income securities.

Investment Philosophy + Process:

The Manager believes that taking a flexible approach to asset allocation allows the team to better manage fixed interest exposure and enhance returns depending on market.

The Fund’s investment and portfolio construction process consists of:

Stage 1: Strategy Formulation: The team ranks the active duration and credit positions of their core Australian Fixed Interest Income strategy.

Stage 2: Risk Calibration: Determine asset allocation using the ranking.

Stage 3: Implementation: Invest in range of cash, fixed interest and higher yielding securities, based on investments decisions from the following:

- Interest rates: (holding longer duration securities versus shorter-dated paper).

- Sectors: (government securities versus non-government given the risk premium).

- Securities: (given the underlying risk/reward, select appropriate non-government securities).

Portfolio Characteristics:

| Portfolio Characteristics | Details |

| Benchmark | 50% Bloomberg Composite 0 + 50% Bloomberg Bank Bill |

| Alpa target p.a.n.m (pree –fees) | 1.0% |

| Minimum suggested time frame | 3 years |

| Alpha source | 30% Rates + 30% Sector / Security selection + 40% Asset Allocation |

| Minimum weighted average credit quality | BBB |

(Source: Janus Henderson)

Investment team:

The Janus Henderson Australian fixed interest team, headed by Jay Sivapalan, is highly experienced and well resourced.

The environmental, social, and governance (ESG) factors are factored into the credit decision-making process. The Manager adheres to the “quality before price” attitude, and hence considers ESG factors to be critical in their four-pillar bottom-up credit analysis. The four pillars are as follows:

- Competitive Advantage and Industry Dynamics

- Financial Risk

- Management Profile

- ESG Risk

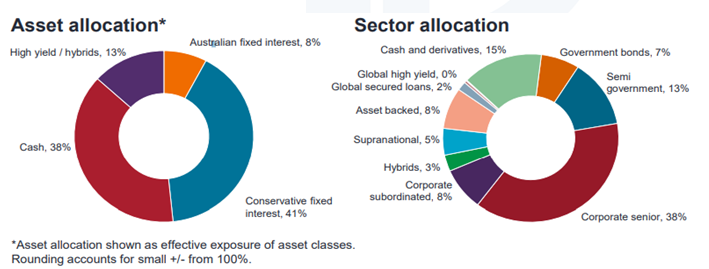

Asset and sector allocation:

(Source: Janus Henders)

Fund Performance(as of august2021:net) and current positioning:

| Percentage | Fund | Benchmark | Outperformance |

| 1-month | -0.09% | 0.05% | -0.14% |

| 3-month | 0.15% | 1.28% | -1.13% |

| 6-month | 0.74% | 2.11% | -1.37% |

| 1-year | 1.28% | 0.56% | +0.72% |

| 3-year (p.a.) | 2.60% | 2.68% | -0.08% |

| 5-year (p.a.) | 2.60% | 2.28% | +0.32% |

| Inception | 4.72% | 3.93% | +0.79% |

(Source: Janus Henderson)

Credit Process:

(Source: Janus Henderson)

Downside Risks:

- Investment strategy selection fails to yield alpha.

- Lead PM departsor significant turnover in the broader investment team

- Manager fails to make the right duration (short or long) call over an extended period of time.

- Credit and interest rate risk

Company Profile:

Janus Henderson is a worldwide asset management company with over 340 investment experts who specialise in all major asset types. Its individual, intermediary, and institutional clients come from all over the world and entrust it with over $500 billion in assets. Over the course of market cycles, Janus Henderson’s commitment to active management allows customers to outperform passive strategies. Its managers use their skills to analyse risk vs reward potential in times of both market calm and growing uncertainty, ensuring customers are on the right side of change.

General Advice Warning

Any advice/ information provided is general in nature only and does not take into account the personal financial situation, objectives or needs of any particular person.