The Fund is led by Crispin Murray, who has over 27 years’ industry experience and is currently the Head of Equity Strategies at Pendal. Mr. Murray is supported by a research team of nineteen, including Mr. Rajinder Singh who has over 17 years’ experience in Australian equities and manages a range of sustainability and ethical funds for Pendal.

The benchmark index is S&P/ ASX300 Accumulation Index.

Downside Risks:

- Market & security specific risk including Australian economic conditions deteriorate.

- The Portfolio Manager/analysts miss-calculate their bottom-up valuation.

- Stock selection fails to yield alpha against the benchmark – Companies which are screened out, such as in materials, energy, gambling, outperform.

- Key man risks with Crispin Murray, Andrew Waddington and Jim Taylor.

Investment Team:

Pendal’s nineteen-member Equity team is one of the largest in the industry. The Fund is managed by Crispin Murray, who is also the Head of Equity and is assisted by Rajinder Singh, who has a combined 44 year’s industry experience.

Fund Performance:

Fund Positioning:

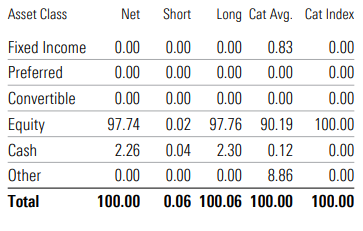

Sector Allocation:

Investment Philosophy & Process:

Investment Philosophy: The Fund’s investment philosophy is based on the belief that good corporate governance and sustainability is a central factor to a company’s longterm success.

Investment Process: The investment process is driven by bottom-up, fundamental research of stocks listed on the Australian Stock Exchange (both large and small cap). The key features of the process are best described in the diagram below. The Manager also utilises a proprietary system as part of its investment process, which includes Analyst Analyser which is a database that captures analyst financial models, valuations and recommendations

About the Fund:

The Pendal Ethical Share Fund is an actively managed portfolio of Australian shares which seeks to ensure that funds are invested in an ethical and socially responsible manner. The Fund invests in companies whose practices and impacts are aligned with an investor’s own social, environmental and ethical preferences and aims to provide a return (before fees, costs and taxes) that exceeds the S&P/ASX 300 Accumulation Index over a 5-year period.

(Source: Banyantree)

General Advice Warning

Any advice/ information provided is general in nature only and does not take into account the personal financial situation, objectives or needs of any particular person.