Process:

AMP Capital Corporate Bond provides exposure to a wide range of credit securities within Australian, global, investment-grade, corporate bond, and high yield. The benchmark changed from the Bloomberg AusBond Credit 0+Yr Index to the Bloomberg AusBond Bank Bill Index in February 2016, reflecting the fund’s capital preservation and income emphasis since 2012. Monthly distributions are announced and reviewed biannually, which helps income-focused investors manage their expectations. Credit analysis is done on two accounts; first, a quantitative and qualitative assessment of the broader industry sector, and second, issuerand security-specific analysis.

The analysis is conducted in line with a “score card” methodology that incorporates fundamentals, technicals, and valuations. The primary weighting is to the valuation and fundamental factors as the team believes this is the primary determinant of a positive outcome for investors over the longer term. The duration view is led by the macro team and is established through a similar score card system, which again considers fundamental, sentiment, and technical factors, with the analyst view of valuation playing a key part. The credit strategy panel, comprising senior investment staff, set the overall credit strategy, risk budget, and sector allocations. However, the ultimate duration and credit exposures are determined by comanagers Sonia Baillie and Nathan Boon.

Portfolio:

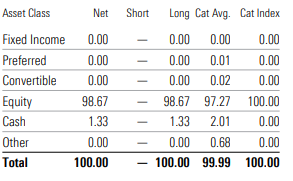

The vehicle chiefly comprises Australian credit, though it does hold around 5% each in US and UK names. The strategy can hold up to 10% in high yield and 15% in unrated bonds but is usually well below these limits. The portfolio is largely BBB and A rated corporate bonds, with the BBB names providing a slightly larger proportion of the fund’s asset value at nearly 44% to October 2021. Following the coronavirus-driven dislocation, the team took opportunistic exposures in long duration REITs and industrials, some of which have seen partial profit taking with significant spread tightening throughout 2021. 2019 saw the fund rotate back into corporate bonds following the late-2018 sell-off.

The team believes credit fundamentals are improving and technicals supportive, but valuations indicate little expectation of further spread compression. It wants to maintain income by holding credit, albeit at a reducing amount to late-2021, also using credit derivatives to insulate from wider spreads. The fund’s duration limits were adjusted from plus or minus 1.5 years versus the old credit benchmark, to absolute terms of zero to 4.5 years in October 2014. The fund has been positioned within a duration range of 0.2-0.8 years since the start of 2017 (0.6 years in October 2021), meaning the sensitivity to rising interest rates is low. FUM has steadily declined over the past few years and currently sits at AUD 855 million as of October 2021.

People:

Sonia Baillie (head of credit) has led this portfolio since October 2017, joined by Nathan Boon (head of credit portfolio management) in March 2018. This group, however, is currently transitioning into the Macquarie fixed-income team as part of AMP Capital’s sale to that organisation; completion is expected by mid-2022, creating some uncertainty. The duo gets significant input from head of macro Ilan Dekell, and a team of analysts spread between Sydney and Chicago. Head of credit research Steven Hur was previously a key member until he left the group in December 2021. The fixed-income team is headed by Grant Hassell, who has more than 30 years of experience, though he is the sole member of this quartet not joining the Macquarie investment team in the same capacity.

Hassell contributes to overall discussions through team meetings and investment committees, acting as the sounding board for the various heads to bring ideas together into a portfolio. While there has been staff turnover among the credit analyst and credit portfolio managers–former managers Jeff Brunton and David Carruthers left in 2014 and 2016, respectively–most key staffers have long tenure. For example, while Baillie was appointed portfolio manager only in 2017, she has been with the team since 2010, has held other senior roles, and worked in the firm’s Asian fixed-income business. Furthermore, AMP Capital has taken steps to improve staff incentives and address staff turnover.

Performance:

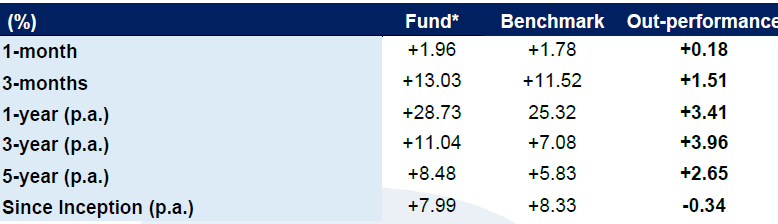

Over the long run, this fund has outdone the Bloomberg AusBond Bank Bill Index and the average credit fund. That’s not necessarily compelling, given the fund has been running substantially more credit and/or duration risk than those yardsticks. Since AMP Capital slashed the fund’s duration, rival credit funds are a more reasonable benchmark looking ahead; the fund’s historically high duration means we also compare the fund’s history against the Bloomberg AusBond Credit Index, where this strategy has underperformed. The fund’s track record has benefited from higher-than-average credit risk, as well as significant interest-rate risk, that has paid off as rates declined to historically low levels. returns, yet three- and five-year returns fail to beat the average category peer. Given declining global interest rates, the fund reduced its distribution in mid-2017 to 0.275% per month, and then 0.25% per month at the beginning of 2018. This continued through 2021 when distributions dropped to 0.175% by year-end, the shop expects it to remain at these compressed levels, barring unforeseen circumstances. The rate peaked at 0.55% per month in 2012, highlighting that while these distribution indications can be helpful in the short run, they should not be relied on for long-term income expectations.

About Funds:

Though a new home will bring positives to AMP Capital Corporate Bond, it also introduces uncertainties for this diversified credit strategy. AMP Capital’s Global Equities and Fixed Interest business is in the midst of a sale to Macquarie Asset Management, which is expected to complete by mid-2022. Head of global fixed income Grant Hassell is leading the integration. The strategy has benchmarked to the Bloomberg Ausbond Bank Bill Index since early-2016, reflecting the income goals with capital stability. This move followed a history of changes, which under Macquarie’s guidance going forward could see further revisions in approach.

(Source: Morningstar)

General Advice Warning

Any advice/ information provided is general in nature only and does not take into account the personal financial situation, objectives or needs of any particular person.