Investment Objective

Vanguard Diversified Growth Index ETF seeks to track the weighted average return of the various indices of the underlying funds in which it invests, in proportion to the Strategic Asset Allocation, before taking into account fees, expenses and tax.

Process

The Vanguard Diversified Index ETF series follows the investment process of the unlisted funds, but with some additional trade-offs of the listed structure, including brokerage costs and variable bid-ask spreads. The methodology starts by defining reasonable investment horizons for each portfolio and allocates to broad asset-class exposures such as equities and fixed interest based on the defensive/growth split. Then, sub asset allocation within classes follows a market-cap weighting approach, while allowing for behavioural biases and regulatory factors specific to each local market. The SAA determination is aided by the Vanguard Capital Markets Model, which forecasts asset-class returns through scenario analysis. An annual review may identify major structural shifts that can lead to a revised SAA.Underlying sector exposures are realised through in-house index-tracking funds.

Portfolio

Vanguard’s straightforward approach applies a strategic asset allocation that is updated periodically and broadly mirrors its equivalent unlisted fund range. Dynamic and tactical asset allocation are not used. Vanguard sticks to the traditional asset classes of equities, fixed interest, and cash, while avoiding alternatives and unlisted assets. The four diversified options are designed to suit different investor objectives and risk profiles. Vanguard Conservative has a defensive/growth split of 70/30, Balanced is 50/50, Growth is 30/70, and High Growth is 10/90.

Performance

In comparison to unlisted peers, all ETFs sit in the top quartile over a trailing three-year time period as at June 2021.

Performance return (%)

Source: Fact Sheet

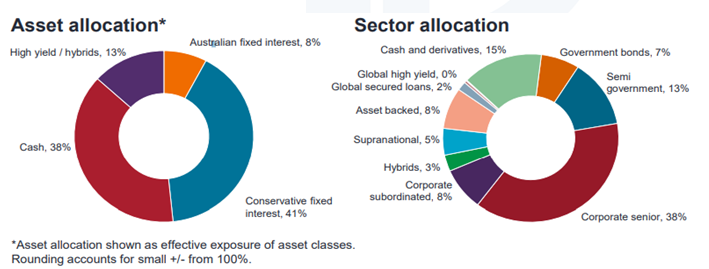

Asset Allocation(%)

Source: Fact sheet

About the fund

The ETF gives investors low-cost access to a variety of sector funds, allowing them to diversify across several asset classes. The Growth ETF is a growth-oriented exchange-traded fund (ETF) created for investors seeking long-term capital growth. A 30% allocation to income asset classes and a 70% allocation to growth asset classes are the goals of the ETF and suitable to buy and hold investors seeking long term capital growth, but requiring some diversification benefits of fixed income to reduce volatility.

(Source: Morningstar)

General Advice Warning

Any advice/ information provided is general in nature only and does not take into account the personal financial situation, objectives or needs of any particular person.