Tag: US Market

Fund Objective

The investment seeks long-term total return, consisting of current income and capital appreciation.

Approach

The strategy targets a yield of 4%-5% and allocates 60%-90% of assets in fixed income, with the remainder in stocks. The team may also employ tactical shifts, vetted by the firm’s tactical trading council, by trading currencies or equity sector indexes, but these can be difficult to execute well consistently. Since introducing a multisleeved approach in early 2018, this strategy has undergone three prospectus benchmark shifts that signal it continues to experiment with its profile. The most recent adjustment (February 2020) decreased the equity exposure by 10 percentage points to 25% in order to make room for a more diversified bond sleeve. Other adjustments include the removal of a REITs sleeve in September 2018, the addition of a securitized bond sleeve in March 2019, and the introduction of an options sleeve in January 2020.

Portfolio

As fixed-income markets have proved richly priced, the portfolio managers cited more attractive capital appreciation and dividends in the equity space, prompting an uptick in the equity holdings to roughly 38% here by September 2021. Within that equity sleeve, technology stocks (Microsoft MSFT is a holding) and healthcare stocks (such as Bausch Health Companies BHC, DaVita DVA, and AbbeVie ABBV) occupied roughly 27% and 17% of assets, respectively.

High-yield bonds dominate the fixed-income portion of the strategy (59% of the portfolio as of September 2021), and it is worth noting that these are more sensitive to equity markets than the investment-grade fare employed by many peers for downside protection in stressed markets. Other bond sleeves here are modest but diversifying relative to the portfolio’s historical profile and include municipal bonds (3%) and securitized bonds (2%).

People

Kandarp Acharya as co manager alongside Margie Patel, who was the sole manager since 2007 but is departing this strategy (though she remains on Allspring Diversified Capital Builder EKBYX) as of Dec. 13, 2021. This move is accompanied by the arrival of quantitative researcher Petros Bocray, a 15-year firm veteran and Acharya’s collaborator on Allspring Asset Allocation EAAIX.

Performance

Over the strategy’s short tenure with its new contours (January 2018 through November 2021), the 5.5% annualized return of its R6 share class modestly outpaced the 5.3% return of the Morningstar Conservative. Target Risk Index and trailed the 6.7% return of its custom benchmark (60% ICE BoA U.S. Cash Pay HY Index, 25% MSCI ACWI, and 15% Barclays Aggregate Index). From an absolute return perspective, the strategy also generated a higher return than the 5.0% median of its typical allocation–15% to 30% equity Morningstar Category peer.This strategy has a riskier profile than many strategies in the category, particularly during stress periods, resulting in risk-adjusted returns (as measured by the Sharpe ratio) that trail all comparative points (typical category peer and benchmark as well as custom benchmark) over the aforementioned period. In three recent stress periods (when energy prices plummeted from June 2015 to February 2016, the 2018 fourth-quarter high-yield sell-off, and the coronavirus-driven market panic of Feb. 20-March 23, 2020), the fund lagged its category index by more than double and trailed its typical peer.

Top 10 Holdings

About the fund

The Fund seeks high current income from investments in income-producing securities. The Fund will normally invest at least 80% of its assets in income producing securities, including debt securities of any quality, dividend paying common and preferred stocks, convertible bonds, and

derivatives. The strategy targets a yield of 4%-5% and allocates 60%-90% of assets in fixed income, with the remainder in stocks. The team may also employ tactical shifts, vetted by the firm’s tactical trading council, by trading currencies or equity sector indexes, but these can be difficult to execute well consistently.

(Source:Morningstar)

General Advice Warning

Any advice/ information provided is general in nature only and does not take into account the personal financial situation, objectives or needs of any particular person.

Business Strategy and Outlook

Several secular trends are affecting Tyson’s long-term growth prospects. While U.S. consumers (86% of fiscal 2021 sales) are limiting their consumption of red and processed meat (69% of Tyson’s sales), they are consuming more chicken (29%). International demand for meat has been strong, and although Tyson’s overseas sales mix is just 14%, it is likely to increase over time, as this is an area of acquisition focus. The beef segment has been a bright spot in Tyson’s portfolio in recent years, as strong international demand, coupled with a drought-induced beef shortage in Australia, has increased the segment’s operating margins to 10% over the past four years from 2% prior to 2016.

Conversely, the chicken segment has suffered from executional missteps that have resulted in structurally higher costs relative to competitors. About 80% of Tyson’s products are undifferentiated (commoditized), so it is difficult for them to command price premiums and higher returns. Although Tyson is the largest U.S. producer of beef and chicken, we do not believe this affords it a scale-based cost advantage, as its segment margins tend to be in line with or below those of its smaller peers.

Financial Strength

Tyson’s financial health as solid and don’t see any issues to suggest that it will be unable to meet its financial obligations. While Tyson generates healthy cash flow and is committed to retaining its investment-grade credit rating, the business is inherently cyclical, with many factors outside of its control. But management has made changes to improve the predictability of earnings. Chicken pricing contracts, which now link costs and prices, and a greater mix of prepared foods (from 10% in 2014 to the current 19%) both serve as stabilizers.

In terms of leverage, net debt/adjusted EBITDA stood at a rather low 1.2 times at the end of fiscal 2021, below Tyson’s typical range of 2-3 times. At the end of September, Tyson held $2.5 billion cash and had full availability of its $2.25 billion revolving credit agreement. Together, this should be sufficient to meet the firm’s needs over the next year, namely about $2 billion in capital expenditures, nearly $700 million in dividends, and $1.1 billion in debt maturities. Management has expressed a commitment to enhancing the income returned to shareholders in the form of its dividend (targeting a 2.0%-2.5% yield over time).

Bulls Say’s

- China’s significant protein shortage resulting from African swine fever should boost near-term protein demand, while the country’s continued moderate increase in per capita consumption of proteins will drive sustainable growth.

- While investor angst over chicken price-fixing litigation has weighed on shares, Tyson’s recently announced settlements materially reduce this overhang.

- In the current inflationary environment, Tyson’s cost pass-through model limits potential profit margin pressure

Company Profile

Tyson Foods is the largest U.S. producer of processed chicken and beef. It’s also a large producer of processed pork and protein-based products under the brands Jimmy Dean, Hillshire Farm, Ball Park, Sara Lee, Aidells, State Fair, and Raised & Rooted, to name a few. Tyson sells 86% of its products through various U.S. channels, including retailers (48%), food service (28%), and other packaged food and industrial companies (10%). In addition, 14% of the company’s revenue comes from exports to Canada, Mexico, Brazil, Europe, China, and Japan.

(Source: MorningStar)

General Advice Warning

Any advice/ information provided is general in nature only and does not take into account the personal financial situation, objectives or needs of any particular person.

Investment Objective

The Fund seeks to track the performance of a benchmark index that measures the investment return of stocks issued by companies located in developed and emerging markets, excluding the United States.

Approach

Vanguard’s portfolio managers use full replication to track the FTSE Global All Cap ex U.S. Index. This benchmark starts with all stocks listed outside of the United States and sorts them by their free-float adjusted market cap. It targets firms that land in the top 98% of each country’s market capitalization. The index uses buffer rules around the cutoff point to keep turnover low, and it applies some additional liquidity requirements to ensure that its holdings are investable. The index weights its final constituents by market cap, which helps further mitigate turnover and trading costs. It reconstitutes semiannually in March and September.

Portfolio

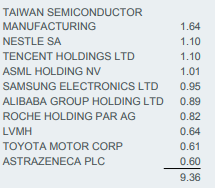

This fund captures the entire foreign stock market. Its comprehensive portfolio effectively diversifies stockspecific risk, with only 9% of assets in its 10 largest holdings. . Sector weightings are comparable, with financial and industrial stocks collectively representing almost one third of the portfolio. Eurozone stocks represent the largest regional allocation, at 20% of the portfolio, while Japan and the United Kingdom make up an additional 16% and 9.4%, respectively. The fund does not hedge its currency risk, so its exposure to currencies like the euro, yen, and pound can add to its volatility. Stocks listed on emerging-markets exchanges account for a little more than 28% of this fund. Allocating to these companies improves the fund’s reach and shouldn’t materially impact its risk or performance. The fund includes small caps but weights its holdings by market cap. So, it leans toward large-cap multinationals, with companies like Taiwan Semiconductor, Nestle, and Samsung among its biggest names.

People

The portfolio managers on this fund are part of Vanguard’s Equity Index Group. Christine Franquin and Michael Perre share responsibility for this fund. They are both principals at Vanguard and captain some of Vanguard’s largest index-tracking funds listed in North America. This duo not only oversees the portfolio but also executes trades on a day-to-day basis

Performance

This fund’s category-relative performance has not stood out from its competitors in the foreign large-blend category. The Admiral share class managed to slightly edge out the average of its peers by 18 basis points annualized over the 10 years through November 2021. The fund’s larger-than-average stake in emerging- markets stocks was a drag during the first few years of that period and partially explains its mediocre showing. The fund’s composition looks a lot like the category average, and it remains fully invested in order to tightly track its target index. That means it tends to post average performance during volatile periods like the coronavirusdriven sell-off in the first quarter of 2020. The fund’s 24% decline was comparable to the loss incurred by the category norm over those three months.

Recent category-relative performance has been stronger. The portfolio led the category average by 67 basis points per year over the trailing three years through November 2021, landing just outside the top third of the category. Poor stock selection in the financials and information technology sectors on the part of some active managers hurt their category-relative performance and boosted the fund’s standing.

Top holdings of the fund

About the fund

The fund tracks the FTSE Global All Cap ex U.S. Index, which includes stocks of all sizes from foreign developed and emerging markets. It weights them by market cap, an approach that benefits investors by capturing the market’s collective opinion of each stock’s value while keeping turnover low. This is one of the broadest portfolios in the foreign large-blend category. Its exceptional diversification mitigates the impact of holding the worst-performing names. It holds more than 7,000 stocks and has only 9% of assets in its 10 largest positions. Its regional composition looks modestly different from a typical fund in the category because it has a larger dose of emerging-markets stocks. But their weight in the portfolio isn’t large enough to materially increase the fund’s risk or compromise its category relative performance.

(Source: Morningstar)

General Advice Warning

Any advice/ information provided is general in nature only and does not take into account the personal financial situation, objectives or needs of any particular person.

IShares Core MSCI Total International Stock ETFs seek to track the investment result of an index composed of large, mid and small capitalization non US equities.

Approach

This fund earns a High Process Pillar rating for capturing the entire opportunity set available to its actively managed competitors in a cost-effective way. BlackRock’s portfolio managers track the MSCI ACWI ex USA Investable Market Index. This benchmark starts with all stocks listed outside of the United States and sorts them by their free-float-adjusted market cap. The final portfolio does not hold every stock in its benchmark index. Instead, the managers buy a representative sample of stocks to match index performance. They nearly fully replicate the large-cap segment and hold a portion of the smaller companies in the index. This reduces the need to trade smaller and less liquid names, which reduces transaction costs.

Portfolio

This fund captures the entire foreign-stock market. Its comprehensive portfolio effectively diversifies stock specific risk, with only 10% of assets in its 10 largest holdings. Sector weightings are comparable, with financials and industrial stocks collectively representing about one third of the portfolio. Country and regional allocations aren’t far off the category average, either. The fund does not hedge its currency risk, so its exposure to currencies like the euro, yen, and pound can add to its volatility. Stocks listed on emerging-markets exchanges account for a little more than 28% of this fund, while a typical competitor has a 10% stake.

People

Industry-leading technology and BlackRock’s global footprint support a strong team of portfolio managers, earning an Above Average People Pillar rating. Alan Mason is head of portfolio management for the Americas and helps manage this portfolio. Rachel Aguirre was promoted to iShares head of product engineering in early 2021 and no longer serves as a manager on this fund. This change should not disrupt the fund’s ability to track its bogy because it retains its three remaining managers and much of their workflow is automated.

Performance

(Source: Factsheet)

Top holdings of the fund (%)

About the fund

The fund tracks the MSCI ACWI ex USA Investable Market Index, which includes stocks of all sizes from foreign developed and emerging markets. It weighs them by market capitalization, an approach that benefits investors by capturing the market’s collective opinion of each stock’s value while keeping turnover low. Market-cap-weighting can be tough to beat because the market tends to do a good job valuing stocks over the long term. Its exceptional diversification mitigates the impact of holding the worst-performing names. It holds more than 4,300 stocks and has only 10% of assets in its 10 largest positions. The fund’s regional composition looks modestly different from the category average.

General Advice Warning

Any advice/ information provided is general in nature only and does not take into account the personal financial situation, objectives or needs of any particular person.