Approach

This UK vehicle has formally adopted a sustainability mandate since April 2021. The investment process starts with hard exclusions, which contains firms with material exposure to weapons, tobacco, coal miners, and oil/gas extraction, among others. The exclusion list was further extended in 2021 to include oil/gas/ nuclear power utilities and firms that the team marked to have “deteriorating” ESG momentum within their sustainability rating framework, but it still accounted for less than 5% of the MSCI AC Asia ex Japan Index, and it hasn’t been seen trigger any material changes to the portfolio over the past year. Dhananjay Phadnis has long favoured quality companies run by strong management teams that can demonstrate cinsistent value creation. It is considered the adoption of a sustainability framework a formalisation of the approach that he has already employed rather than a material change. Phadnis focuses on a firm’s competitive advantages, management quality, potential for improvement on ESG practice, and valuations in stock selection. The end portfolio consists of 50-70 names, which typically are fundamentally sound businesses trading below their intrinsic values and out-of-favour stocks with turnaround catalysts. Sector and country allocations are a residual of stock selection, though weights must stay within 10 percentage points of the index. Phadnis has done an excellent job extracting performance out of the strategy’s risk budget, and his investment savvy brings a further edge to the approach’s execution. Overall, the strategy maintains Process rating of High.

Portfolio

Dhananjay Phadnis increased the portfolio’s exposure to financials to 28.1% as of December 2021 from 19.3% a year ago, which represented a 9.4% overweighting compared with the MSCI AC Asia ex Japan Index. He added to AIA, despite it being a major underperformer in 2021. At Analysts’ January 2022 meeting, Phadnis remained positive on the insurer’s growth outlook, noting that it managed to expand its agent head count and branch out into new provinces in China when other Chinese insurers experienced difficulties in maintaining their agency force in 2021. Conversely, his conviction in Ping An Insurance waned given its slower-than-expected agency reform and its questionable decision of buying a majority stake in bankrupt Founder Group, and he has therefore exited his position. Meanwhile, the December 2021 portfolio continued to have an overweight position in information technology, where its 27.3% stake was above the index’s 25.8%. Phadnis liked SK Hynix, believing that the chipmaker’s acquisition of Intel’s NAND unit will enhance its competitiveness in the global memory market and that it has better corporate governance among Korean companies. Within consumer discretionary (16.1%), Phadnis initiated a stake in Meituan in July 2021 when its valuation became more compelling amid the regulatory crackdown. He believed the food delivery giant’s business model can adapt to new regulatory standards, noting its pricing power and efficient delivery network in the segment.

People

Dhananjay Phadnis brings 20 years of investment experience and has led this strategy’s UK and Luxembourg-domiciled vehicles since November 2013 and March 2015, respectively. He joined Fidelity in 2004 as an analyst and covered a variety of sectors before being promoted to portfolio manager in 2008. He has since posted excellent results across the single-country and regional mandates under his management, though he now focuses on this sustainable Asia equity strategy, which includes the USD 1.2 billion, Luxembourg-domiciled Fidelity Asian Equity fund that Phadnis took over from former manager Suranjan Mukherjee in August 2021. Phadnis had a total AUM of USD 6.1 billion as of December 2021. It is alleged Phadnis is one of the best Asian equity managers, who has consistently showcased astute investment savvy and a great passion for investing. Director of sustainable investing Flora Wang has been the strategy’s assistant portfolio manager since February 2021, when it formally adopted a sustainability mandate. Most of Wang’s contributions currently lie in the ESG integration front, including engaging with companies and identifying materiality issues. She is also gradually developing her fundamental stock-picking skills under Phadnis’ mentorship, and it is monitored how her role evolves. Phadnis is supported by Fidelity’s deep Asia Pacific ex Japan team of 58 analysts who average nine years of experience and six years with Fidelity. The team has showed greater stability since 2020 and has further grown with six additions in 2021 through September. Overall, the strategy continues to merit a People rating of High.

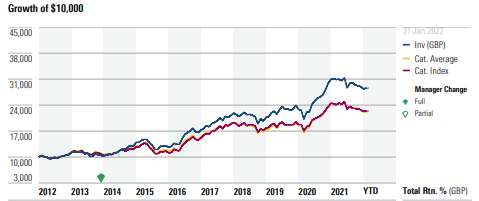

Performance

Lead manager Dhananjay Phadnis has delivered excellent results since he took over the UK-domiciled vehicle in November 2013. Through 31 Jan 2022, the W Acc share class returned 12.3% per year (in pound sterling), beating the MSCI AC Asia ex Japan Index’s 8.57% gain, the MSCI Emerging Markets Asia Index’s 8.86% gain, and 96% of its Asia ex Japan equity category peers. Its standard deviation was slightly higher than the indexes but in line with typical peers, resulting in robust risk-adjusted results. Indeed, the share class’ Sharpe ratio of 0.58 during the same period outpaced both indexes and 97% of peers. The outperformance was primarily driven by strong stock selection in China and India, with consumer discretionary, communication services, and financials contributing from a sector perspective.

Phadnis’ quality bias and prudent risk management helped buoy the strategy’s relative performance in the 2021 down market. Although the W Acc share class lost 3.2% last year, it outperformed the MSCI AC Asia ex Japan Index by 64 basis points and ranked in the 48th percentile among peers. The vehicle primarily benefited from solid stock picks in the communication services and industrials sectors, with Bharti Airtel, NAVER, and Titan Wind Energy being some of the top contributors. The underweightings in Alibaba and Tencent and not owning Pinduoduo also helped, as they plunged on the back of heightened regulatory crackdowns in 2021. Conversely, stock picks in financials and healthcare detracted.

About Fund:

Fidelity International Limited is mainly owned by management and members of the Johnson family, who founded US-based Fidelity Investments. The entities have been separate since 1980, and though there are some similarities, in practice there is only limited alignment between the two. There were a number of personnel changes in 2018-19, including a change in CEO and the CIOs of equities, fixed-income, and multiasset, but the composition of senior management has been relatively stable since. More important, these changes do not seem to have negatively affected day-to-day investment activities, and on the whole, the initiatives undertaken by new management seem sensible.

(Source: Morningstar)

General Advice Warning

Any advice/ information provided is general in nature only and does not take into account the personal financial situation, objectives or needs of any particular person.