Tag: Australian Market

On 28 October 2021, MXT announced a Unit Purchase Plan (UPP) proposing to issue 220.8m new units at a price of $2.00 per unit. The Trust is targeting to raise ~$441.6m. While the Trust maintains the flexibility to accept applications in excess of the target raise amount, applications in excess of this amount may also be scaled back.

The Offer closed on 30 November 2021 with an Issue Date of 3 December 2021. New units are expected to commence trading on 6 December 2021.

Capital raised will be invested in accordance with the investment mandate and target return of the Trust.

MXT targets a return of the RBA cash rate plus 3.25% p.a. (currently 3.35% p.a. net of fees) through the economic cycle, with income distributions intended to be paid monthly. Since listing on the ASX in October 2017, MXT has delivered a net return of 5.15% pa.

Net Asset Value of metrics Master Income Trust is $1,573,565,708. Current Unit Price is $2.07.

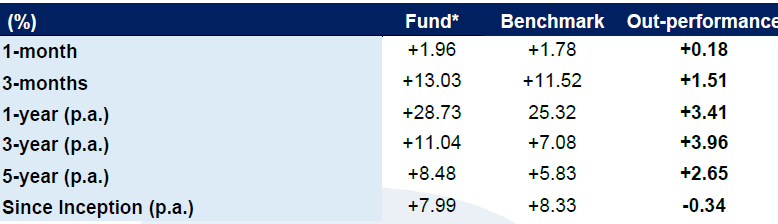

Performance

Company Profile

The Investment Objective of the Metrics Master Income Trust is to provide monthly cash income, low risk of capital loss and portfolio diversification by actively managing diversified loan portfolios and participating in Australia’s bank‐dominated corporate loan market. The Manager seeks to implement active strategies designed to balance delivery of the Target Return, while seeking to preserve investor.

(Source: FN Arena, Bloomberg, MXT)

General Advice Warning

Any advice/ information provided is general in nature only and does not take into account the personal financial situation, objectives or needs of any particular person.

Investment strategy

The Fund uses a multi-step investment process for constructing the Fund’s investment portfolio that combines top-down sector allocation with bottom-up individual stock selection. Top-down sector allocation is determined through a systematic evaluation of listed and direct property market trends and conditions. Bottom-up stock selection is driven by proprietary analytical techniques to conduct fundamental company analysis, which provides a framework for security selection through an analysis of individual securities independently and relative to each other. Investment return objective The Fund aims to outperform (after management costs) the S&P/ASX 300 Property Accumulation Index over rolling three year periods.

Investment return objective

The Fund aims to outperform (after management costs) the S&P/ASX 300 Property Accumulation Index over rolling three year periods.

Downside Risks

- Deterioration in the Australian economy especially the property market (fundamentals deteriorate). Rising bond yields negatively impacting pricing.

- The Portfolio Manager/analysts miss-calculate their bottom-up valuation

- Key person risks in Mr. Pica (however, the CBRE investment team is relatively large and capable of succession planning).

Fund Performance (as at 31 May 2021)

(Source: UBS)

Fund Positioning: Top 5 Holdings – Overweights & Underweights (as at 31 May 2021)

(Source: UBS)

Investment Process

The Fund uses an investment process that combines in-depth top-down and bottom- up fundamental market research with a disciplined and systematic approach to portfolio construction and risk management. The Portfolio Manager’s bottom-up approach integrates both quantitative and qualitative research to identify individual securities where the real estate is undervalued and represents the most compelling investment opportunities. The securities research process incorporates several factors including:

- Property visits – the Portfolio Manager utilises its local presence to gauge the quality and location of the real estate, assessing properties and capital expenditure needs at the property level.

- Management meetings – the Portfolio Manager assesses the management team’s alignment with shareholders; determines the depth and experience of the team; and judges their ability to articulate and execute their strategy.

- Modelling – the Portfolio Manager generates cash flow earnings projections; performs net asset value analysis; and analyses the capital structure.

About the fund

The UBS Property Securities Fund (portfolio managed by CBRE while Distributed by UBS) is a portfolio of mainly Australian Real Estate Investment Trusts that the investment team believes are being undervalued by the market, based on the in-house assessment of the company’s future cashflows. The Fund aims to outperform (after management costs) the S&P/ASX 300 Property Accumulation Index over rolling five-year periods

(Source: Banyantree)

General Advice Warning

Any advice/ information provided is general in nature only and does not take into account the personal financial situation, objectives or needs of any particular person.

The Fund is led by Crispin Murray, who has over 27 years’ industry experience and is currently the Head of Equity Strategies at Pendal. Mr. Murray is supported by a research team of nineteen, including Mr. Rajinder Singh who has over 17 years’ experience in Australian equities and manages a range of sustainability and ethical funds for Pendal.

The benchmark index is S&P/ ASX300 Accumulation Index.

Downside Risks:

- Market & security specific risk including Australian economic conditions deteriorate.

- The Portfolio Manager/analysts miss-calculate their bottom-up valuation.

- Stock selection fails to yield alpha against the benchmark – Companies which are screened out, such as in materials, energy, gambling, outperform.

- Key man risks with Crispin Murray, Andrew Waddington and Jim Taylor.

Investment Team:

Pendal’s nineteen-member Equity team is one of the largest in the industry. The Fund is managed by Crispin Murray, who is also the Head of Equity and is assisted by Rajinder Singh, who has a combined 44 year’s industry experience.

Fund Performance:

Fund Positioning:

Sector Allocation:

Investment Philosophy & Process:

Investment Philosophy: The Fund’s investment philosophy is based on the belief that good corporate governance and sustainability is a central factor to a company’s longterm success.

Investment Process: The investment process is driven by bottom-up, fundamental research of stocks listed on the Australian Stock Exchange (both large and small cap). The key features of the process are best described in the diagram below. The Manager also utilises a proprietary system as part of its investment process, which includes Analyst Analyser which is a database that captures analyst financial models, valuations and recommendations

About the Fund:

The Pendal Ethical Share Fund is an actively managed portfolio of Australian shares which seeks to ensure that funds are invested in an ethical and socially responsible manner. The Fund invests in companies whose practices and impacts are aligned with an investor’s own social, environmental and ethical preferences and aims to provide a return (before fees, costs and taxes) that exceeds the S&P/ASX 300 Accumulation Index over a 5-year period.

(Source: Banyantree)

General Advice Warning

Any advice/ information provided is general in nature only and does not take into account the personal financial situation, objectives or needs of any particular person.

Investment Objective:

The Fund aims to provide investors with the performance of an index, before fees and expenses, composed of the 200 largest Australian securities listed on the ASX.

Portfolio Objective:

Can be used as a core Australian equities exposure.

Low cost access (relative to fund managers managing domestic portfolios) to the 200 largest companies on the ASX in a single fund.

Positives:

• Low cost exposure to broader market, without having to pick individual stocks.

• Given the concentration in the Australian market, investors can use this ETF as a core holding whilst selecting lesser known stocks to drive portfolio alpha.

Negatives:

• Deterioration in Australian economy.

• Aggressive increase in global bonds yields, leading to equity risk repricing.

• Parent company experiences financial stress or negative corporate governance event.

ETF Performance:

ETF Positioning:

About the Company:

BlackRock is a global asset manager listed on the New York Stock Exchange. BlackRock has a comprehensive range of products and services across asset classes, geographies and investment strategies with 135.

(Source: Banyantree)

General Advice Warning

Any advice/ information provided is general in nature only and does not take into account the personal financial situation, objectives or needs of any particular person.

Investment Thesis

- Currently under a takeover target.

- Structural challenges – consumers moving away from carbonated soft drinks (CSD).

- Increased competitive pressures from other beverage companies or margin pressure/erosion from supermarket chains.

- Cost pressure eroding margins, including the NSW container deposit scheme.

- CCL not being able to push through price increases to clients.

- CCL has a strong global brand portfolio with diversified product offering.

- Strong growth in NZ, Indonesia and PNG.

- Management is focused on cost out and reinvestment, growing efficiency and margins as a result.

Key Risks

- CCL unable to sustain the turnaround especially in International segments.

- Company meets or exceeds its full year guidance.

- Increased competitive pressures.

- Cost pressure eroding margins, including the NSW container deposit scheme.

- CCL not being able to push through price increases to clients.

- International segment unable to deliver growth.

Key Financial Results

- Volumes for the year were down -4.2% over pcp and revenue declined -3.5% to $2.94bn with a more pronounced decline in ongoing EBIT (down -14.7% to $362.6m with margin down -170bps to 12.3%) due to changes in channel and pack mix (multi-serve PET and multipack cans increasing and demand for immediate consumption offerings decreasing) as consumer behaviour responded to Covid-19 lockdown measures. Management have seen a recovery in volumes starting 2H20, with strong momentum carried into January 2021 trading.

- The Company was able to achieve market share gains in the non-alcohol ready to drink (NARTD) market which grew during the year, delivering NARTD volume share gains of +0.7% with Coca-Cola Trademark increasing its volume share by +0.4%.

Company Profile

Coca-Cola Amatil (CCL) manufactures, distributes and sells carbonated soft drinks along with still and mineral waters, fruit drinks, ready-to-drink coffee and tea and flavoured milk drinks. CCL also rents and services commercial refrigeration equipment to food/beverage manufacturers.

(Source: BanyanTree)

General Advice Warning

Any advice/ information provided is general in nature only and does not take into account the personal financial situation, objectives or needs of any particular person.

Business Strategy and Outlook

Magellan is an active manager of listed equities and infrastructure. The firm has had considerable success in growing funds under management, or FUM, owing to its superior track record of outperformance, product expansion initiatives, and strong distribution capabilities.

The firm has a fundamental, high-conviction investment approach. Its flagship Global strategy has historically tilted toward IT, e-commerce platforms, and consumer franchises; preferring large, developed market multinationals. FUM have been attracted by consistently achieving excess returns with lower volatility and drawdowns relative to peers.Magellan’s products are well-distributed. Its funds are featured across platforms, included in model portfolios, and are well-rated.

There is a focus on targeting retail investors, with product expansion an increasingly common driver of growth. As per Morningstar analyst, Magellan has built the foundations for ongoing earnings growth, supported by its economic moat, product variety, and historically strong track record. Regardless, the potential earnings upside from these positive traits will take time to manifest.

Magellan Loses Largest Mandate, but Sell-Off Way Overdone

Morningstar analyst reduced its fair value estimate for Magellan Financial Group by 25% to AUD 38 per share, following client the termination of its mandate with its largest client, St James’s Place, or SJP. As per the viewpoint of Morningstar analyst, most of Magellan’s institutional clients hired the group to deliver returns of about 10% per year and focus on downside protection. It is an investment undertaking Magellan has always communicated to the market, and a hurdle it consistently surpassed, with institutional returns averaging 18% per year over the last five years. As Magellan’s recent underperformance has only begun since November 2020, it was believed that institutional clients would negotiate for lower fees rather than terminate Magellan. Regretfully, this has not transpired in SJP’s case.

Financial Strength

Magellan is in sound financial health.The firm has a conservative balance sheet with no debt, with its financial position also boosted by solid operating cash flows. As of June 30, 2021, Magellan had cash and equivalents of about AUD 212 million and financial investments with a net fair value of around AUD 453 million mainly invested in its own unlisted funds and listed shares. This should provide it with enough liquidity to cope with most market conditions. Its high dividend payout ratio of: (1) 90%-95% of the net profit after tax of its core funds management business before performance fees; and (2) annual performance fee dividend in the range of 90%-95% of net crystallised performance fees aftertax reflects the capital-light nature of asset management.

Bull Says

- The majority of Magellan’s earnings come from a few large funds, meaning it has a high reliance on key investment personnel and the performance of its main funds. Should key people leave, or its main funds underperform for a sustained period, outflows could be material.

- There is increasing competition from other active international equity managers and new international equity funds from incumbents.

- The firm faces fee pressure from the increasing popularity of lower-cost alternatives, such as indextype products and ETFs.

Company Profile

Magellan Financial Group is an Australia-based niche funds manager. Established in 2006, the firm specialises in the management of equity and infrastructure funds for domestic retail and institutional investors. Magellan has been particularly successful in winning mandates from global institutional investors. Current FUM is split across global equities, infrastructure and Australian equities

(Source: Morning Star)

General Advice Warning

Any advice/ information provided is general in nature only and does not take into account the personal financial situation, objectives or needs of any particular person.