Approach

This strategy aims to track the Bloomberg Ausbond Composite 0+ Index with a tracking error of 0.05% per year or less (before fees). IShares is typically able to achieve full replication of the government-bond component in the portfolio because of ample liquidity and breadth. To alleviate liquidity challenges, the firm uses stratified sampling to acquire corporate and supranational exposures–an industry-standard approach, but one in which iShares excels thanks to its sophisticated global trading systems and experienced team. When the team can’t buy all the bonds in the index at a reasonable price, it will instead buy a basket of bonds that has similar credit and duration risks within allowable tolerance ranges. The team also employs strategies like securities lending to generate additional returns, helping to offset the performance drag from factors like fees and trading costs. IShares’ scale further minimises trading costs; a large active book and the firm’s ETF business allow for cross-trades and wide broker access. IShares thus executes trades cheaply, which is crucial in index fund management. It’s worth noting that Bloomberg’s index assumes distributions earn no interest, whereas iShares may accrue interest on its distribution cash balances. This may cause some tracking error, but ultimately it is a positive tailwind.

Portfolio

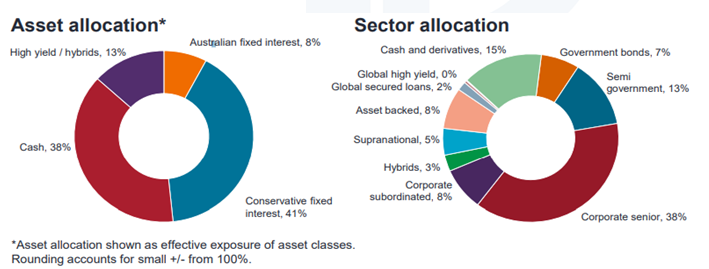

This strategy aims to fully replicate the Bloomberg AusBond Composite 0+ Index. Factoring cost, liquidity, and existing diversification if it doesn’t make sense to own all the bonds on issue, it will use stratified sampling to buy a basket of bonds with similar credit and duration risks. As of 28 Feb 2022, the index was composed of government and semigovernment bonds (85%), supranationals (5%), and corporate bonds (9%). The fund invests in high-quality bonds, with AAA rated debt constituting 71% of the benchmark’s quality exposure. Banks and other financials issue most of the credit in the index. The fund’s duration continues to increase with the benchmark as yields mostly hovered around historic lows barring the recent spike, up from 4.95 years at October 2016 to 5.8 years at 28 Feb 2022. The lengthening duration is a result of Commonwealth Government Bonds being issued at longer tenures, such as 30 years. But it means the fund faces the risk of rising yields globally, when we would expect active managers in this space to outperform their long-duration passive peers. Overall credit quality and appropriate diversification make this strategy an appropriate core exposure.

Performance: In terms of Annualised and Cumulative basis

Top 10 Holdings of the fund

About the fund

The fund aims to provide investors with the performance of the Bloomberg Aus Bond Composite 0+ Yr Index SM, before fees and expenses. The index is designed to measure the performance of the Australian bond market and includes investment grade fixed income securities issued by the Australian Treasury, Australian semi-government entities, supranational and sovereign entities and corporate entities.

(Source: Morningstar)

General Advice Warning

Any advice/ information provided is general in nature only and does not take into account the personal financial situation, objectives or needs of any particular person.