BetaShares FTSE RAFI Australia 200 ETF QOZ offers distinctive exposure to Australian equities based on a fundamental index. QOZ aims to track the FTSE RAFI Australia 200 Index before fees and expenses. Conforming to a contrarian methodology, the index construction is driven by a four-factor method developed by US-based Research Affiliates. The five-year average of the four metrics (book value, sales, cash flow, and dividend) are used to build a portfolio with reliable but currently undervalued stocks.

Approach

QOZ aims to track the FTSE RAFI Australia 200 Index before fees and expenses. This index eliminates the traditional market-cap-weighted index approach where portfolio weight depends on share price. Instead, QOZ favours stocks with a larger “economic footprint.” The index comprises the top 200 companies listed on the ASX, as measured by four equally weighted fundamental measures: sales, cash flow, dividends, and book value. Five-year averages are used for the first three factors, with the latest available book value applied. Stocks are weighted based upon an equally weighted composite score of these four metrics.

Portfolio

Market-cap-weighted Australian equity benchmarks are dominated by large sectors and companies. A handful of very large financial services and materials companies compose a significant slice of the overall pie. QOZ shares these characteristics, but instead of weighting by market cap, it uses an index based on fundamental metrics in which stocks with bigger economic footprints (earnings, sales, dividends, and book value) receive more prominence.

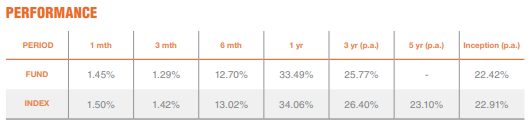

Performance

Value-titled strategies have faced difficult times over the past decade. The returns have been typically overshadowed by the conventional growth-oriented strategies. However, it should be noted that such factor skews undergo cycles and may see an upturn when the macroeconomic environment changes. As at December 2021, QOZ delivered an annualised five-year return of 8.2% against the S&P/ASX 200’s 9.8%. The year 2016 was a period of contrasting halves as valuations dipped in the first half and quickly raced back and beyond in the latter half. The fund significantly outperformed the broader index over this period, delivering returns of 18.3%. The rally continued in 2017, and the fund ended with over 11.3% returns during the year. In 2018, US-China trade wars surfaced, causing global unrest in the equity markets. As such, the fund witnessed a sharp drawdown in the year’s final quarter.

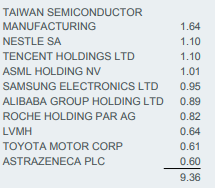

Company Profile

Cimic is Australia’s largest contractor, providing engineering, construction, contract mining services to the infrastructure, mining, energy, and property sectors. The business structure consists of construction, contract mining, public-private partnerships, and property, along with 45%-owned Habtoor Leighton. Cimic has exited its Middle East business. ACS/Hochtief owns 76% of Cimic.

(Source: Morningstar)

General Advice Warning

Any advice/ information provided is general in nature only and does not take into account the personal financial situation, objectives or needs of any particular person.