IShares Core MSCI Total International Stock ETFs seek to track the investment result of an index composed of large, mid and small capitalization non US equities.

Approach

This fund earns a High Process Pillar rating for capturing the entire opportunity set available to its actively managed competitors in a cost-effective way. BlackRock’s portfolio managers track the MSCI ACWI ex USA Investable Market Index. This benchmark starts with all stocks listed outside of the United States and sorts them by their free-float-adjusted market cap. The final portfolio does not hold every stock in its benchmark index. Instead, the managers buy a representative sample of stocks to match index performance. They nearly fully replicate the large-cap segment and hold a portion of the smaller companies in the index. This reduces the need to trade smaller and less liquid names, which reduces transaction costs.

Portfolio

This fund captures the entire foreign-stock market. Its comprehensive portfolio effectively diversifies stock specific risk, with only 10% of assets in its 10 largest holdings. Sector weightings are comparable, with financials and industrial stocks collectively representing about one third of the portfolio. Country and regional allocations aren’t far off the category average, either. The fund does not hedge its currency risk, so its exposure to currencies like the euro, yen, and pound can add to its volatility. Stocks listed on emerging-markets exchanges account for a little more than 28% of this fund, while a typical competitor has a 10% stake.

People

Industry-leading technology and BlackRock’s global footprint support a strong team of portfolio managers, earning an Above Average People Pillar rating. Alan Mason is head of portfolio management for the Americas and helps manage this portfolio. Rachel Aguirre was promoted to iShares head of product engineering in early 2021 and no longer serves as a manager on this fund. This change should not disrupt the fund’s ability to track its bogy because it retains its three remaining managers and much of their workflow is automated.

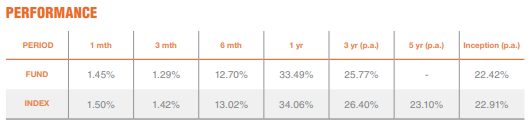

Performance

(Source: Factsheet)

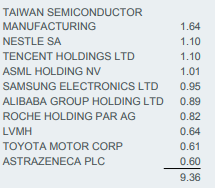

Top holdings of the fund (%)

About the fund

The fund tracks the MSCI ACWI ex USA Investable Market Index, which includes stocks of all sizes from foreign developed and emerging markets. It weighs them by market capitalization, an approach that benefits investors by capturing the market’s collective opinion of each stock’s value while keeping turnover low. Market-cap-weighting can be tough to beat because the market tends to do a good job valuing stocks over the long term. Its exceptional diversification mitigates the impact of holding the worst-performing names. It holds more than 4,300 stocks and has only 10% of assets in its 10 largest positions. The fund’s regional composition looks modestly different from the category average.

General Advice Warning

Any advice/ information provided is general in nature only and does not take into account the personal financial situation, objectives or needs of any particular person.