Process:

The Walter Scott investment team executes a patient investment process, undertaking rigorous fundamental research to identify quality names that can deliver superior long-term returns. It earns an Above Average Process rating. The process starts with an initial screen of businesses that can deliver at least 20% cash flow return on investment over a full market cycle. The managers have an active watchlist of approximately 250 companies they closely monitor, and the team undertakes fundamental bottom-up analysis, assessing factors such as competitive position, industry dynamics, profitability, balance-sheet strength, financial model, and quality of management.

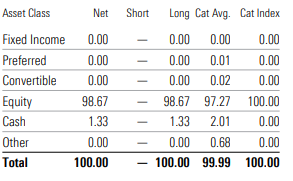

Portfolio:

The team constructs a relatively concentrated portfolio that usually has 40-60 names. Adequate diversification is maintained by limiting position sizes to a maximum of 5 percentage points, but typically they don’t exceed 4% of the portfolio. The group’s long-term quality focus results in the strategy exhibiting a bias toward mega-cap stocks, though it does hold some mid-cap names. Historically, the strategy has exhibited significant country-level bets. It is typically underweighted in the United States relative to the MSCI World Index. At the sector level, the strategy favours tech, healthcare, and consumer cyclical stocks, while having a large underweighting in financial services.

People:

An experienced, stable team that works together well leads to a High People rating. Investment decision-making at subadvisor Walter Scott is team-based. All investments, new and existing, are discussed and debated until there is unanimous agreement by the research team. Stability and experience characterize Walter Scott’s investment team, with members boasting impressive experience and tenures with the firm. More than half of the investment team members have spent their entire investment careers at the company. In 2021, one of the joint portfolio managers, Yuanli Chen, left, a rare departure. Long-term cohead of research Alan Edington moved to a new position, Responsible Investment.

Performance:

The strategy has sported strong results from its late-December 2006 launch through 2021. The I shares’ 9.4% annualized gain exceeded its MSCI World Index prospectus benchmark’s 7.4% and edged the typical world large-stock growth peer. However, it’s lost a bit of an edge against a more growth-oriented benchmark, with the MSCI World Growth Index up 10% annualized during the period.

(Source: Morningstar)

Price:

Analysts find it difficult to analyse expenses since it comes directly from the returns. Analysts expect that it would be able to deliver positive alpha relative to its category benchmark index.

(Source: Morningstar) (Source: Morningstar)

About Funds:

With a focus on investing for the long term, the portfolio consistently favors technology, healthcare, and consumer discretionary names while being significantly underweight in financial services and energy. The strategy won’t always lead the way in buoyant markets. It landed behind the MSCI World Index benchmark in 2021. The investment seeks long-term total return. To pursue its goal, the fund normally invests at least 80% of its net assets, plus any borrowings for investment purposes, in stocks. The fund’s investments will be focused on companies located in the developed markets. Examples of “developed markets” are the United States, Canada, Japan, Australia, Hong Kong and Western Europe. It may invest in the securities of companies of any market capitalization. The fund’s sub-investment adviser, Walter Scott & Partners Limited (Walter Scott), seeks investment opportunities in companies with fundamental strengths that indicate the potential for sustainable growth.

(Source: Morningstar)

General Advice Warning

Any advice/ information provided is general in nature only and does not take into account the personal financial situation, objectives or needs of any particular person.