Tag: Australian Market

Investment Objective

The investment objectives of the Fund are to achieve attractive risk-adjusted returns over the medium to long-term, while reducing the risk of permanent capital loss.

Investment Process

The investment objective of the strategy is two-fold:

- Achieve attractive risk adjusted returns over the medium to long-term (translates to 9% p.a. net of fees long-term target)

- Minimise the risk of permanent capital loss (downside protection)

The Magellan Global Fund aims to invest in ‘outstanding companies’ at attractive prices, while also managing investment risk through a comprehensive understanding of the macroeconomic and broader environment. ‘Outstanding’ in this context refers to companies that are able to “sustainably exploit competitive advantages in order to continually earn returns on capital that are materially in excess of their cost of capital.” As such, the Fund is not deterred by companies that may be perceived as trading expensively (e.g. at high multiples), so long as their underlying businesses are outstanding, and share prices are assessed to be trading at a discount to intrinsic value.

The investment team assesses each stock via five quality criteria (economic moat, re-investment potential, business risks, agency risks, and ESG factors). This analysis reduces the universe to around 300 stocks which then undergo detailed bottom-up analysis. The team discusses the results to determine stocks that will be recommended to the investment committee. Investments will need to have a margin of safety (discount to intrinsic value) to enter the portfolio.

The stringent quality criteria result in a concentration in global franchises, information technology, global infrastructure and niche financial services companies. Analysts build discounted cash flow models to determine the intrinsic value of each company. A “conviction scoring matrix” is also used to ensure that each company is consistently evaluated both relative to peers and on a standalone basis.

Portfolio

Investment Team

In February 2022, CIO and Lead Portfolio Manager Hamish Douglass took, effective immediately, a medical leave of absence for personal reasons and mental health issues. It is important to note, the Company does expect Mr Douglass to return in due course when he is healthy to return.

In June 2022, the Manager announced that Mr. Douglass will cease to be a permanent member of Magellan’s staff on 15 June 2022 and will commence the consultancy role on 1 October 2022. Mr. Douglass will be available to the investment team, as required by them, to share his insights including his views on macroeconomic and geo-political matters.

In the interim, Chris Mackay (Magellan’s co-founder) will step in and oversee the portfolio management of Magellan’s global equity retail funds and global equity institutional mandates. Chris is a highly experienced Portfolio Manager with a solid track record in global equities. Further, Nikki Thomas has re-joined Magellan as a Co-portfolio manager of Magellan’s global equity strategies. Nikki was due to commence in March however due to this announcement, she agreed to start 7th February. Nikki is a highly regarded Portfolio Manager with over 20 years of experience in the management of global equity portfolios. Nikki was instrumental in the development of the Magellan investment team’s processes in 2006, and she has a deep knowledge of Magellan’s investment universe. Her experience and relationships with investment advisers and consultants will add further depth to the investment team. Chris Mackay will be working with Deputy CIO Dom Giuliano, Nikki Thomas, Arvid Streimann and Chris Wheldon in respect of the co-management of the global equity and high conviction retail funds and institutional mandates.

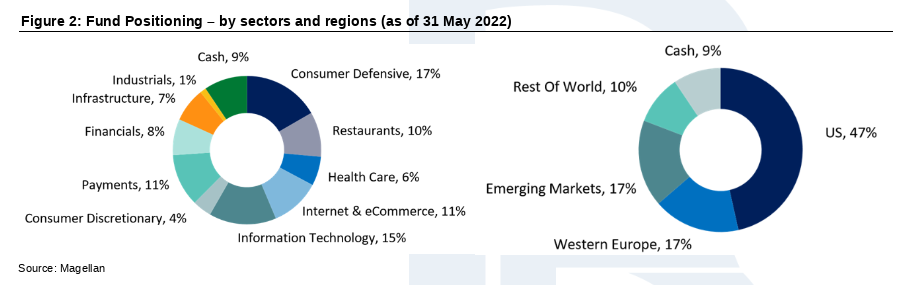

Fund Performance and Positioning

About Fund:

The Magellan Global Fund (Unhedged) is a concentrated, currency unhedged, benchmark unaware international equities strategy that typically contains 20-40 stocks. The objectives are capital preservation and reduction of downside volatility risk, while having a minimum return objective of 9% p.a. (net of fees).

(Source: Banyantree)

DISCLAIMER for General Advice: (This document is for general advice only).

This document is provided by Laverne Securities Pty Ltd T/as Laverne Investing. Laverne Securities Pty Ltd, CAR 001269781 of Laverne Capital Pty Ltd AFSL No. 482937.

The material in this document may contain general advice or recommendations which, while believed to be accurate at the time of publication, are not appropriate for all persons or accounts. This document does not purport to contain all the information that a prospective investor may require. The material contained in this document does not take into consideration an investor’s objectives, financial situation or needs. Before acting on the advice, investors should consider the appropriateness of the advice, having regard to the investor’s objectives, financial situation, and needs. The material contained in this document is for sales purposes. The material contained in this document is for information purposes only and is not an offer, solicitation or recommendation with respect to the subscription for, purchase or sale of securities or financial products and neither or anything in it shall form the basis of any contract or commitment. This document should not be regarded by recipients as a substitute for the exercise of their own judgment and recipients should seek independent advice.

The material in this document has been obtained from sources believed to be true but neither Laverne and Banyan Tree nor its associates make any recommendation or warranty concerning the accuracy or reliability or completeness of the information or the performance of the companies referred to in this document. Past performance is not indicative of future performance. Any opinions and or recommendations expressed in this material are subject to change without notice and, Laverne and Banyan Tree are not under any obligation to update or keep current the information contained herein. References made to third parties are based on information believed to be reliable but are not guaranteed as being accurate.

Laverne and Banyan Tree and its respective officers may have an interest in the securities or derivatives of any entities referred to in this material. Laverne and Banyan Tree do and seek to do business with companies that are the subject of its research reports. The analyst(s) hereby certify that all the views expressed in this report accurately reflect their personal views about the subject investment theme and/or company securities.

Although every attempt has been made to verify the accuracy of the information contained in the document, liability for any errors or omissions (except any statutory liability which cannot be excluded) is specifically excluded by Laverne and Banyan Tree, its associates, officers, directors, employees, and agents. Except for any liability which cannot be excluded, Laverne and Banyan Tree, its directors, employees and agents accept no liability or responsibility for any loss or damage of any kind, direct or indirect, arising out of the use of all or any part of this material. Recipients of this document agree in advance that Laverne and Banyan Tree are not liable to recipients in any matters whatsoever otherwise; recipients should disregard, destroy or delete this document. All information is correct at the time of publication. Laverne and Banyan Tree do not guarantee reliability and accuracy of the material contained in this document and are not liable for any unintentional errors in the document.

The securities of any company(ies) mentioned in this document may not be eligible for sale in all jurisdictions or to all categories of investors. This document is provided to the recipient only and is not to be distributed to third parties without the prior consent of Laverne and Banyan Tree.

Business Strategy & Outlook:

A key attraction of Hotel Property Investments is favorable lease terms that provide predictable above-inflation rental income from long-term leases to joint venture entity Queensland Venue Company, which is an agreement between supermarket giant Coles and private equity owned (Kohlberg Kravis Roberts) Australian Venue Company. AVC manages the day-to-day operations of the hotels, with Coles needing the hotel licenses to operate its liquor retailing business under restrictive Queensland laws. There is ongoing uncertainty around Coles’ longer-term strategy regarding its liquor business following competitor Woolworth’s decision to exit its liquor and hotel businesses. Close to 90% of Hotel Property’s freehold properties are in Queensland, predominantly pubs that are leased to QVC. The joint venture leases generate about 90% of Hotel Property’s rental income.

Since annual rents are not linked to earnings, investors do not generally benefit from the upside of stronger pub operating performance and face the downside risk of the joint venture not renewing leases on poorly performing pubs. Although this risk has been substantially alleviated due to the renewal of most leases for an extended 10- to 15-year period. The further trade-off is the defensive nature of the long lease terms, and strong tenants that generate above-inflation rentals with low maintenance costs. Most properties are on attractive triple-net lease terms where the tenant is responsible for most expenses other than land tax in Queensland, which recently increased. The portfolio currently has a weighted average lease term of about 10 years. Hotel Property is the ultimate holder of hotel licenses on most properties. These licenses allow the sale of liquor at up to three detached bottle shops within 10 kilometers of the main premises. Licenses revert to Hotel Property at the end of the lease term with respect to most pubs. Where the joint venture owns the license but opts to terminate the lease, Hotel Property has right of first refusal over the license at a preset price tied to trading data at that time.

Financial Strengths:

Hotel Property is in sound financial health, with gearing (debt less cash/total assets less cash) of about 39% in early 2022, well below covenant gearing of 60% and within its target gearing of between 35% and 45%. It is also comfortably meeting its interest cover covenant of 1.5 times, with current interest cover (earnings before interest and tax/interest expense) of above 3.9 times. Debt maturity profile is fairly long at 4.6 years. The recent precipitous fall in interest rates should alleviate interest costs because about 40% of its debt is on floating rates.

Bulls Say:

- Hotel Property Investments’ distribution yield is higher than most Australian REIT peers, supported by most contracted annual rental increases averaging the lesser of 2 times CPI or 4%.

- Rental income is underpinned by long lease terms.

- Liquor and most gaming licenses are retained by Hotel Property when leases expire. This is a contingent asset that should be a draw-card for potential pub tenants in the absence of adverse regulatory changes.

Company Description:

Hotel Property Investments is an Australian REIT with a portfolio of freehold pub properties primarily in Queensland. Its portfolio is almost exclusively leased to Queensland Venue Company on triple-net long-term leases where the tenant is responsible for outgoings (except land tax in Queensland), resulting in relatively low maintenance expenses. Most leases also provide for annual rental increases typically at the lower of 4% or two times the average of the last five years consumer price index.

(Source: Morningstar)

DISCLAIMER for General Advice: (This document is for general advice only).

This document is provided by Laverne Securities Pty Ltd T/as Laverne Investing. Laverne Securities Pty Ltd, CAR 001269781 of Laverne Capital Pty Ltd AFSL No. 482937.

The material in this document may contain general advice or recommendations which, while believed to be accurate at the time of publication, are not appropriate for all persons or accounts. This document does not purport to contain all the information that a prospective investor may require. The material contained in this document does not take into consideration an investor’s objectives, financial situation or needs. Before acting on the advice, investors should consider the appropriateness of the advice, having regard to the investor’s objectives, financial situation, and needs. The material contained in this document is for sales purposes. The material contained in this document is for information purposes only and is not an offer, solicitation or recommendation with respect to the subscription for, purchase or sale of securities or financial products and neither or anything in it shall form the basis of any contract or commitment. This document should not be regarded by recipients as a substitute for the exercise of their own judgment and recipients should seek independent advice.

The material in this document has been obtained from sources believed to be true but neither Laverne and Banyan Tree nor its associates make any recommendation or warranty concerning the accuracy or reliability or completeness of the information or the performance of the companies referred to in this document. Past performance is not indicative of future performance. Any opinions and or recommendations expressed in this material are subject to change without notice and, Laverne and Banyan Tree are not under any obligation to update or keep current the information contained herein. References made to third parties are based on information believed to be reliable but are not guaranteed as being accurate.

Laverne and Banyan Tree and its respective officers may have an interest in the securities or derivatives of any entities referred to in this material. Laverne and Banyan Tree do and seek to do business with companies that are the subject of its research reports. The analyst(s) hereby certify that all the views expressed in this report accurately reflect their personal views about the subject investment theme and/or company securities.

Although every attempt has been made to verify the accuracy of the information contained in the document, liability for any errors or omissions (except any statutory liability which cannot be excluded) is specifically excluded by Laverne and Banyan Tree, its associates, officers, directors, employees, and agents. Except for any liability which cannot be excluded, Laverne and Banyan Tree, its directors, employees and agents accept no liability or responsibility for any loss or damage of any kind, direct or indirect, arising out of the use of all or any part of this material. Recipients of this document agree in advance that Laverne and Banyan Tree are not liable to recipients in any matters whatsoever otherwise; recipients should disregard, destroy or delete this document. All information is correct at the time of publication. Laverne and Banyan Tree do not guarantee reliability and accuracy of the material contained in this document and are not liable for any unintentional errors in the document.

The securities of any company(ies) mentioned in this document may not be eligible for sale in all jurisdictions or to all categories of investors. This document is provided to the recipient only and is not to be distributed to third parties without the prior consent of Laverne and Banyan Tree.