Investment Thesis:

- Competent leadership team with a proven track record of delivering strong growth (Strong top-line momentum driven by strong support of accountants and bookkeepers with annualised monthly recurring revenue increasing at CAGR 32% and strong subscriber growth with positive LTV (Lifetime Value) trends (over FY15-19, ANZ LTV grew at CAGR 48% and International LTV grew at CAGR 65%)).

- Solid product offering that is secure, scalable and efficient technology which is competing against competitors with technology that has legacy issues. We note that XRO’s small business platform is an ecosystem of more than 700 connected apps backed by a community of more than 50,000 users of XRO’s API developer tools. Going forward the Company could potentially increase its revenue by monetising its platform in other ways like charging third party app developers.

- Potential for meaningful acquisitions to fill gaps in product capability. In our view, the Company is well positioned to make acquisitions going forward (given its balance sheet and funding status).

- The Company continues to focus on cloud accounting, and we see significant upside potential in the sector given the fact that the current levels of small business cloud accounting adoption globally is estimated to be less than 20% of the total market or opportunity across English-speaking countries in which the Company operates.

Key Risks:

- Decrease of migration to cloud software.

- Currency headwinds due to weakening of NZ$ relative to AUD, USD and Pound.

- Deteriorating sentiment if the economy and IT spending weakens.

- Excessive competition from other established players like Intuit leading to loss of market share.

- Inability to extract higher operational efficiencies as the Company scales up.

- Issues in gaining market share especially in markets with established incumbents.

Key highlights:

- Improving trends in key metrics – (1) subscriber growth; (2) higher ARPUs (average revenue per user); and (3) lower churn.

- A key catalyst for XRO’s share price going forward will be execution and growth in North America.

- Despite relatively mature markets in New Zealand and Australia, XRO’s subscriber growth in 1H22 in both markets (NZ +16% and Aus +22%) was a standout from our perspective.

- The Company finished 1H22 with net cash position of NZ$125m and has total available liquidity of NZ$1.2bn.

- Operating revenue was up +23% (or up +26% in constant currency) to NZ$505.7m, with total subscribers up +23% to 3.0m and ARPU (average revenue per user) up +5% to NZ$31.32

- The financial position for different markets of Xero are as follows:

- Australia: Segment revenue was up +22% to NZ$225m, with net additions up +24% and subscribers up +22% to 1.24m.

- New Zealand: Segment revenue was up +13% to NZ$72m, with net additions up +55% and subscribers up +16% to 480,000.

- United Kingdom: Segment revenue was up +33% to NZ$133m, with net additions up +160% and subscribers up +23% to 785,000.

- North America: Segment revenue was up +5% to NZ$30m, with net additions up +130% and subscribers up +23% to 308,000.

- Rest of World: Segment revenue was up +72% to NZ$46m. with net additions up +136% and subscribers up +48% to 201,000.

Company Description:

Xero Ltd (XRO) is a software as a service (SaaS) company, engaged in the provision of a platform for online accounting and business services to small businesses and their advisors. The Company operates through two operating segments: Australia and New Zealand (ANZ), and International (UK + North America + Rest of the World).

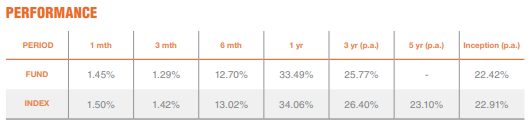

(Source: Banyantree)

General Advice Warning

Any advice/ information provided is general in nature only and does not take into account the personal financial situation, objectives or needs of any particular person.