Author: Aayushi Swami

Process:

Davis maintains a relatively concentrated portfolio of 50-60 stocks but seeks to minimize the magnitude of sector or factor bets. He also tends to add and trim positions aggressively as they become more or less attractive according to analyst models, a tendency that benefits when stock prices mean revert. While Davis’ artful approach has some appeal, it doesn’t have a discernible edge relative to its competition.

Portfolio:

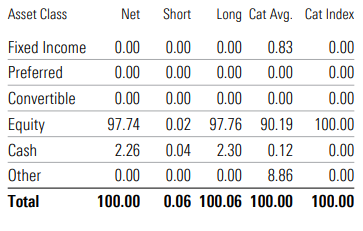

This portfolio finds a balance between differentiation and careful risk management. It held 51 stocks at the end of September 2021, significantly less than the 140-180 it used to have when it had three independently managed sleeves. However, manager Scott Davis’ desire to let stock selection drive results leads to only modest sector and industry tilts relative to its S&P 500 benchmark. Davis also considers factor exposure when building the portfolio. For instance, he increased the portfolio’s stake in financials companies toward the end of 2020 to bolster its exposure to cheaper, more cyclical stocks to help offset its lack of exposure to the energy sector.

The portfolio has historically leaned a bit more toward a growth style, and that still rings true. It displayed a slight growth bias relative to the benchmark as of October, sporting higher valuation metrics such as price/ sales and faster trailing revenue- and earnings-growth rates.

People:

This strategy continues to rely heavily on J.P. Morgan’s core research team, but it is now led exclusively by Scott Davis, who oversaw the strongest-performing sleeve of this formerly multi-managed offering. Davis became a named manager in August 2014, inheriting a 10% slice of the strategy, but quickly saw his share grow, most notably after manager Thomas Luddy stepped down at the end of 2017. Davis continues to leverage the ideas of J.P. Morgan’s core research team, which consists of 23 analysts with extensive industry experience.

Performance:

A good portion of the fund’s success came in 2020, which skews the trailing return figures a bit. Its 26.7% gain in 2020 outpaced the benchmark by over 8 percentage points, the best calendar year since Davis debuted. The fund’s case over other time periods is weaker: It outperformed the bogy about 51% of the time on a rolling one-year basis since Davis joined.

(Source: jpmorgan.com)

Price:

Analysts find it difficult to analyse expenses since it comes directly from the returns. Analysts expect that it would be able to generate positive alpha relative to its benchmark index.

(Source: Morningstar)

About Funds:

The investment objective of this fund is to achieve a return in excess of the US equity market by investing primarily in US companies. It uses a research-driven investment process that is based on the fundamental analysis of companies and their future earnings and cash flows by a team of specialist sector analysts.

(Source: Morningstar)

General Advice Warning

Any advice/ information provided is general in nature only and does not take into account the personal financial situation, objectives or needs of any particular person.

Investment Thesis:

- Number one player in the domestic market (approximately 50% market share), with only one major competitor (Huon Aquaculture Group). This could see rational pricing behaviour, which should be positive for both companies.

- High barriers to entry (assets, desired temperatures and regulatory licences are difficult to obtain).

- Initiatives like selective breeding programs and investments in infrastructure appear to be paying dividends, with more recent generations of TGR’s salmon showing more robust growth than their predecessors.

- Given the complex nature of salmon farming, TGR is unlikely to have its dominant position as an Australian leading salmon farmer seriously threatened in the foreseeable future.

- Addition of prawns into TGR’s product portfolio brings diversification benefits to the Company’s risk profile.

- Growth in prawns represents material upside for group earnings.

Key Risks:

- Impact on production due to adverse weather conditions and diseases.

- The De Costi subsidiary presents an opportunity for diversification; however, execution and competitive risks remain.

- Potential review of chemical colouring in salmon may lead to further negative publicity and undermine demand for salmon.

- Cost pressures or cost blowout could deteriorate margins significantly given the large cost base relative to earnings (EBITDA).

- Irrational competitive behaviour (domestic and international markets).

- Negative media reports on the sustainability of the Tasmanian salmon industry.

- Regulatory risks regarding Federal, State and Local laws and regulations regarding the leases, licenses, permits and quotas which may affect TGR’s operations.

Key highlights:

- TGR’s 1H21 revenue was up on volume growth but EBIT and NPAT fell by -2.7% and -7.8% on pcp, respectively, amid materially negative returns from the export market due to Covid19.

- Interim dividend was down -22.2% to 7cps.

- Operating cash flows remained strong despite negative movements in working capital and declining salmon prices.

- Total revenue increased +6.6% over pcp to $292.48m, with sales volume growth for salmon up +16.2% and prawns up +786.4%, which was more than offset by materially negative returns from the export market given the impact of reduced global pricing and an appreciating AUD/USD exchange rate, leading to operating EBIT falling -2.7% over pcp to $46.78m

- Balance sheet further strengthened with available committed debt facilities extended by $100m to $509.2m (including Receivables Purchasing Facility), secured to April 2023

- The Board declared an unfranked interim dividend (vs 25% franked in pcp) of 7cps, down -22.2% over pcp and announced a DRP with a -2% discount.

- Segment revenue are as follows:

- Salmon: Segment revenue increased +6.7% over pcp, with decline of -8.7% to $12.47/hog kg in average price (domestic down -2.6% and export down -18%) more than offset by +16.2% increase in volume (domestic up +1.3% and export up +74.3%).

- Prawns: Operating EBITDA/kg (pre AASB 16) declined -47% over pcp to $3.05, as earlier harvest to optimize Christmas sales led to decrease in size

Company Description:

Tassal Group (TGR) is Australia’s largest vertically integrated seafood/aquaculture company. Based in Tasmania, TGR is engaged in hatching, farming, processing, sale and marketing of Atlantic salmon and ocean trout. Tassal is also undergoing investments to enter the prawns market. The company’s products are distributed in Australia, Japan and other international markets.

(Source: Banyantree)

General Advice Warning

Any advice/ information provided is general in nature only and does not take into account the personal financial situation, objectives or needs of any particular person.

Investment Thesis

- Relative to major banks, BEN trades at fair value in our view, on 13.2x one-year forward price to earnings, 0.9x price to book and dividend yield of ~5.0%.

- Strong franchise model with funding predominately by way of deposits.

- Expected low levels of impairment charges (especially as a low interest rate environment helps customers and arrears).

- Continued strong cost discipline, improving efficiency and boosting performance.

- Advanced accreditation in progress (which may improve ROE).

- Potential pressure on net interest margins as competition intensifies, with major banks in a low interest rate environment.

- Leading in terms of customer satisfaction and net promoter metrics, which are increasingly key in a period where trust is paramount.

Key Risks

- Intense competition for loan growth, combined with further discounting.

- Volatility in Homesafe earnings.

- Increase in bad and doubtful debts or increase in provisioning. It is to monitor the asset quality of Rural Bank and Great Southern portfolios.

- Funding pressure for deposits and wholesale funding.

FY21 Results Highlights

- Statutory net profit of $243.9m, up +67.3%. Cash earnings after tax of $219.7m, up 1.9%. Cash earnings per share of 41.4cps declined -5.5%. Total income was $849.0m, up +3.3%. Operating expenses of $517.4m, down -3.1% as BEN was able to drive cost reductions across the business.

- Net interest margin of 2.30% was down 7bps, reflecting “active pricing and volume management for lending and deposits, despite lower lending rates due to a mix of growth and competitive new business rates”. Core BEN NIM of 1.97% was up +6bps on 2H20 NIM of 1.93%. Management noted the December 2020 exit NIM was -3bps lower, which again highlights margin pressure remains from front book/back book repricing. However, we expect this to be offset by favourable funding costs.

- Bad and doubtful debts of $19.5m, declined – 15.9%, and comprises 6bps of gross loans. This was a solid outcome and we are likely to continue to see lower BDDs in the near-term. However, we remain cautious of this trend further out as government assistance starts to pull back.

- Common Equity Tier 1 of 9.36%, improved 36 basis points on the pcp, above APRA’s ‘unquestionably strong’ benchmark.

Company Profile

Bendigo and Adelaide Bank Ltd (BEN) offers a variety of banking and other financial services including internet banking, housing finance, retail and business banking, commercial finance, funds management, treasury and foreign exchange services, superannuation and trustee services.

(Source: BanyanTree)

General Advice Warning

Any advice/ information provided is general in nature only and does not take into account the personal financial situation, objectives or needs of any particular person.

Investment Thesis

- Leveraged to changes in the USD.

- Solid assets with reserve/resource.

- New acquisitions provide upside (resource and operational improvement).

- Strong management team with significant mining expertise.

- Strong balance sheet

- Company has a good track record on shareholder return

Key Risks

- Deterioration in global gold supply & demand equation.

- Deterioration in gold prices.

- Production issues, delay or unscheduled mine shutdown.

- Adverse movements in AUD/USD

FY21 Results Highlights

- Solid first half results with gold sales coming in at the top end of Company’s guidance and management noting that they remain on track to meet full year guidance. Relative to the pcp, revenue was up +34% to $1.1bn, with average gold price realized up +17% (AUD terms) and gold sold (ounces) up +21% over the period. Operating earnings (EBITDA) were up +47% to $472.2m and underlying NPAT of $194.4m was up +63%.

- Company declared an interim dividend of 9.5cps (fully franked), which was in line with payout policy of 6% of revenue.

- Underlying free cash flow was strong, up +94% to $225.7m.

- Strong balance sheet, with $672m in liquidity available, consisting of cash, bullion and investments of $372m and $300m in undrawn facilities.

- NST currently has approx. 10% of annualised production hedged over the next 3 years (350kozs at $2,128/oz). NST has been focusing on reducing its hedge book so that it can potentially participate in higher gold prices.

- FY21 guidance was unchanged on what was provided at the FY20 results

Company Description

Northern Star Resources Limited (Northern Star) is a gold production and exploration company with a Mineral Resource base of 10.2 million ounces and Ore Reserves of 3.5 million ounces, located in highly prospective regions of Western Australia and the Northern Territory. NST is the third largest gold producer in Australia. The Company also recently acquired a gold mine in Alaska.

General Advice Warning

Any advice/ information provided is general in nature only and does not take into account the personal financial situation, objectives or needs of any particular person.

Investment Thesis:

- Attractive dividend yield of 5.4%.

- Market-leading position in New Zealand. Dominant market share in Mobile, Broadband and is the leader in IT Services.

- Strong capacity for growth demonstrated across all segments, with IT expected to continue to be a key driver as more consumers and businesses migrate to the Cloud.

- Investments in Broadband and the roll-out of 4.5G should see its lagging broadband segment improve.

- Multi-product offerings provide interesting points of differentiation from other telco providers.

- Implementation of “Agile” leading to further cost reductions and operating efficiencies.

- Increasing customer demand for higher-margin cloud-based services.

- Increases in ARPU growth and connections despite weak industry conditions

- SPK still commands a strong market positions and has the ability to invest in technologies and areas which could provide room for growth.

Key Risks:

- Unsuccessful migration of copper wire customers resulting in earnings drag in May due to weather conditions.

- More competition in its Mobile and Broadband segments leading to aggressive margin contraction, especially as products become commoditized.

- Risk of cost blowout (for instance in network upgrades or maintenance).

- Churn risk.

- Balance sheet risk (including credit ratings risk) should earnings decline due competitive and structural risks.

- Reduced flexibility and increased net debt if unable to fund total dividend by earnings per share

- Any network disruptions/outages.

Key highlights:

- SPK’s earnings were negatively impacted by Covid-19 with ongoing loss of mobile roaming revenues and lower growth broadband and prepaid markets.

- EBITDA was up +0.4% to $502m, despite Covid-19 impacts, offset from strong cost controls.

- Margin of 27.4% was 60bps lower than the pcp. NPAT was -11.4% lower to $148m, driven by a $29m increase in depreciation and amortisation charges resulting from the shorter asset lives of new digital technologies, and higher depreciation related to customer and property leases.

- Operating expenses declined $30m, or -2.3%, offsetting revenue declines

- NPAT was -11.4% lower to $148m, driven by a $29m increase in depreciation and amortisation charges resulting from the shorter asset lives of new digital technologies, and higher depreciation related to customer and property leases.

- Free cash flow of $113m, was up $63m over the pcp on tight management of working capital resulting in higher cash conversion rate of 102%.

Company Description:

Spark New Zealand Ltd (SPK) is a New Zealand based telecommunications company. SPK’s key services are the provision of telephone lines, mobile telecommunications, broadband services and IT services. Its key product offerings are Spark Home, Mobile & Business, Spark Digital, Spark Ventures, and Spark Connect. The Company operates four main segments: (1) Spark Home, Mobile & Business; (2) Spark Digital; (3) Spark Connect & Platforms; and (4) Spark Ventures & Wholesale.

(Source: Banyantree)

General Advice Warning

Any advice/ information provided is general in nature only and does not take into account the personal financial situation, objectives or needs of any particular person.