The Fund provides exposure to investment grade securities from around the globe while incorporating PIMCO’s ESG screening framework. The strategy can be used as a core bond holding in client portfolios who have an ESG bias. The PIMCO Global Bond Fund is in attraction due to the well-resourced / experienced investment team and PIMCO’s well established investment process. PIMCO’s ESG framework involves three stages: (1) Exclude (restrictions on certain sectors). (2) Evaluate (best in class ESG issuers + prime engagement candidates). (3) Engage (engage issuers to improve ESG related business practices).

Downside Risk

- Interest rate risk (bond prices and yields are inversely related).

- Credit risk (the risk of downgrades or even default) & inflation risk.

- Personnel risk – significant turnover among the 3 lead PMs.

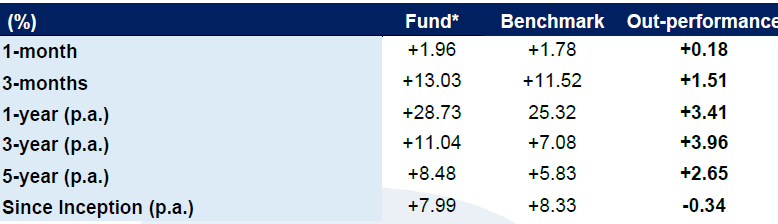

Fund Performance (As at Aug, 2021)

Investment Process

PIMCO applies a wide range of strategies including Duration analysis, Credit analysis, Relative Value analysis, Sector Allocation and Rotation and individual security selection. The Manger looks to make active decisions with a long-term focus and avoid extreme swings in duration or maturity with a view to creating a steady stream of returns. The Manager has designed and structured a global investment process that includes both top-down and bottom-up decision-making. The first and most important step in the firm’s process is to get the long-term view correct. The figure below provides a summary of the key elements in the investment process.

Secular analysis: The Manager considers its secular analysis as critical to the investment process, with the firm devoting three days every year to a “Secular Forum”. At this forum, the firm formulates PIMCO’s outlook for global bond markets over the next three to five years. Selected members of the investment staff are assigned secular topics to monitor, including monetary and fiscal policy, inflation, demographics, technology, productivity trends, and global trade. Secular researchers tackle their subjects on a global basis and approach them over a multi-year horizon. At the forum the researchers present their findings to all of the firm’s investment professionals.

Decision making: Post Secular and Economic Forums, the Investment Committee (senior portfolio managers) develop major strategies that serve as a model for all portfolios using a consensus-based approach. The IC utilises top-down analysis provided by the forums as well as bottom-up input from specialists who focus on various fixed income sectors and the regional portfolio committees. The Investment Committee sets targets for portfolio characteristics such as duration, yield curve exposure, convexity, sector concentration and credit quality and ensures themes are consistently applied across all portfolios. The portfolio management group including the PIMCO Global Strategy team, through the incorporation of the Investment Committee’s model portfolio characteristics, will then construct the Fund.

About the fund

The ESG Global Bond Fund is an actively managed portfolio of global fixed interest investment which incorporates PIMCO’s ESG screening. The portfolio predominantly invests in governments, corporate, mortgage and other global fixed interest securities.

(Source: Banyantree)

General Advice Warning

Any advice/ information provided is general in nature only and does not take into account the personal financial situation, objectives or needs of any particular person.