Tag: Australian Market

Approach

The index tracks the performance of the exchange-listed equity securities of companies across the globe that (i) engage in providing cyber defence applications or services as a vital component of its overall business or (ii) provide hardware or software for cyber defence activities as a vital component of its overall business. The fund invests at least 80% of its total assets in the component securities of the index and in ADRs and GDRs based on the component securities in the index.

Portfolio

An ETF Model Portfolio is a carefully selected portfolio of exchange traded funds (ETFs) and other exchange traded products constructed and managed by a professional investment manager.

The investment manager typically also provides regular reporting on the portfolio’s performance, along with ongoing communication on changes to the portfolios, the rationale for doing so, and broader commentary on the micro and macro environment.

BetaShares offers four series of model portfolios, each of which seeks to achieve capital growth and income streams through a careful blending of asset classes, including Australian and international equities, bonds, cash and commodities. The models are constructed using ETFs and other exchange-traded products, resulting in institutional-quality portfolios that are cost-effective, highly diversified, transparent, and simple to explain to clients.

- Strategic asset allocation (SAA) ETF model portfolios: Built using forward-looking 10-year expected returns and risk for a diversified range of major asset classes.

- Dynamic asset allocation (DAA) ETF model portfolios: Utilise return/risk parameters from SAA, rebalanced quarterly based upon BetaShares’ modelling of asset class misevaluations, risk objectives and economic considerations.

- Dynamic Income model portfolios: Aim to produce total returns that are similar to the dynamic ETF models, but are weighted towards income rather than capital growth.

- Pension Risk-Managed Model Portfolios: Uses ETPs that aim to provide enhanced income returns and/or less volatile returns through a systematic risk-management overlay.

People

dam O’Connor is a member of the BetaShares Distribution team responsible for supporting Institutional and Intermediary Broker and Adviser channels. Prior to joining BetaShares, Adam worked in stockbroking and advisory with Bell Potter Securities. Alex is responsible for leading the strategy and overall management of the business. Prior to co-founding BetaShares, Alex was closely involved in the establishment and development of several leading Australian financial services businesses including Pengana Capital and Centric Wealth. Alistair is a member of the BetaShares Distribution team, responsible for supporting Institutional and Intermediary Broker channels, as well as supporting the firm’s capital markets activities. Annabelle is a member of the BetaShares marketing team focusing on social media and content. Anthony is responsible for supporting the investment and operations functions at BetaShares. Anton is BetaShares’ internal legal adviser and is also responsible for managing the compliance function. Ben is responsible for supporting the distribution of BetaShares funds to advisers across the Victoria and South Australia regions. Benjamin is a member of the BetaShares Distribution team, responsible for assisting with client inquiries.

Brendan is responsible for growing and servicing BetaShares Adviser business clients across Western Australia. In this role, Brendan is focused on educating advisers about the role and benefits of ETF’s and SMA’s in client portfolios and sharing updates on the expanding range of strategies available across the BetaShares product suite. Cameron’s responsibilities span supporting all distribution channels and working alongside the portfolio management team. Prior to joining BetaShares, Cameron was a portfolio manager at Macquarie Asset Management, and was responsible for the structuring and management of Macquarie’s listed and unlisted structured product offering. Cameron’s other experience includes Head of Product at Bell Potter Capital, working on JP Morgan’s Equity Derivatives desk and at Deloitte Consulting.

Performance

The ETFMG Prime Cyber Security ETF was the first ETF to focus on the cyber security industry. It tracks an index of companies involved in hardware, software and services, classifying the underlying stocks as either infrastructure or service providers. Top holdings include Cisco Systems, Akamai and Qualys.

About Fund

FactSet ETF Analytics Scoring Methodology is one of the first wide-ranging and robust methodologies for evaluating, comparing and contrasting exchange-traded funds. The researchers and analysts at FactSet developed the system. The result of thousands of hours of research, debate and testing, FactSet ETF Analytics Scoring Methodology provides a comprehensive structure for investors to analyze ETFs. FactSet’s quantitative system allows an investor to evaluate a fund at a glance, aggregating a sweeping range of detailed, often-difficult-to-obtain data points. FactSet’s Letter Grade combines the Efficiency and Tradability score evaluating costs to the investor. The combined score is assigned a letter grade (A-F) providing an institutional-caliber view on how well run and how liquid the ETF is. Efficiency includes risks, which are potential costs. Funds that minimize these risks can be more efficient.

(Source: Betashare)

DISCLAIMER for General Advice: (This document is for general advice only).

This document is provided by Laverne Securities Pty Ltd T/as Laverne Investing. Laverne Securities Pty Ltd, CAR 001269781 of Laverne Capital Pty Ltd AFSL No. 482937.

The material in this document may contain general advice or recommendations which, while believed to be accurate at the time of publication, are not appropriate for all persons or accounts. This document does not purport to contain all the information that a prospective investor may require. The material contained in this document does not take into consideration an investor’s objectives, financial situation or needs. Before acting on the advice, investors should consider the appropriateness of the advice, having regard to the investor’s objectives, financial situation, and needs. The material contained in this document is for sales purposes. The material contained in this document is for information purposes only and is not an offer, solicitation or recommendation with respect to the subscription for, purchase or sale of securities or financial products and neither or anything in it shall form the basis of any contract or commitment. This document should not be regarded by recipients as a substitute for the exercise of their own judgment and recipients should seek independent advice.

The material in this document has been obtained from sources believed to be true but neither Laverne and Banyan Tree nor its associates make any recommendation or warranty concerning the accuracy or reliability or completeness of the information or the performance of the companies referred to in this document. Past performance is not indicative of future performance. Any opinions and or recommendations expressed in this material are subject to change without notice and, Laverne and Banyan Tree are not under any obligation to update or keep current the information contained herein. References made to third parties are based on information believed to be reliable but are not guaranteed as being accurate.

Laverne and Banyan Tree and its respective officers may have an interest in the securities or derivatives of any entities referred to in this material. Laverne and Banyan Tree do and seek to do business with companies that are the subject of its research reports. The analyst(s) hereby certify that all the views expressed in this report accurately reflect their personal views about the subject investment theme and/or company securities.

Although every attempt has been made to verify the accuracy of the information contained in the document, liability for any errors or omissions (except any statutory liability which cannot be excluded) is specifically excluded by Laverne and Banyan Tree, its associates, officers, directors, employees, and agents. Except for any liability which cannot be excluded, Laverne and Banyan Tree, its directors, employees and agents accept no liability or responsibility for any loss or damage of any kind, direct or indirect, arising out of the use of all or any part of this material. Recipients of this document agree in advance that Laverne and Banyan Tree are not liable to recipients in any matters whatsoever otherwise; recipients should disregard, destroy or delete this document. All information is correct at the time of publication. Laverne and Banyan Tree do not guarantee reliability and accuracy of the material contained in this document and are not liable for any unintentional errors in the document.

The securities of any company(ies) mentioned in this document may not be eligible for sale in all jurisdictions or to all categories of investors. This document is provided to the recipient only and is not to be distributed to third parties without the prior consent of Laverne and Banyan Tree.

Approach

Realindex uses a systematic index method employing four equally weighted measures of a company’s economic size to rank and weight stocks in the portfolio. These criteria are adjusted sales, cash flow, and dividends and latest available adjusted book value. Additional earnings quality, near-term value, and debtcoverage filters act to reduce exposure to stocks with greater uncertainty. A signal was also introduced in November 2015 that downweights stocks with negative momentum and overweights stocks with positive momentum. As a part of its endeavor to improve current metrics, Realindex has more recently refined the book value metric to factor in intangibles as well by adjusting it with capitalize R&D and marketing expenses. The filters have contributed to a value bias and tilt to established companies that typically trade at a discount. This alternative approach to traditional index investing aims to eliminate the relationship between portfolio weighting and over/undervaluation associated with weighting a portfolio by market cap. The portfolio is rebalanced quarterly, resulting in average annual turnover of about 15%. The team handles all aspects of research, portfolio management, implementation, and execution with a focus on minimizing trading costs and market impact.

Portfolio

Realindex constructs a diversified, value-leaning portfolio. The strategy’s factors and price filters can lead to some differences relative to the more commonly used S&P/ASX 200 Accumulation Index. For example, the portfolio typically has lower price/book ratios and higher dividend yields. Realindex’s absolute weighting to most sectors remains relatively stable because the fundamental size characteristics tend not to fluctuate wildly unlike the sector weights fluctuation in market-cap benchmarks. Other deviations have been a historic tilt away from healthcare and real estate. Relative to the category index, S&P/ASX 200 Index, the strategy is value-focused and yield-oriented. Large-cap bias is apparent in the portfolio, but it is relative to the category average. As of November 2021, the portfolio was overweight in financial services and underweight in resources and healthcare. Realindex’s portfolio, traditionally, has remained quite similar to market-cap benchmarks overall. Historically, active share has hovered around 20%.

People

Realindex has been through a significant phase of transition in the past couple of years bought about by the end of the partnership with RAFI and the exit of a few senior portfolio managers. This has provided an opportunity for Realindex to revamp its overall team structure and bring on experienced investment professionals. The experienced David Walsh has joined as the head of investment, leading portfolio management and research, which Scott Hamilton leads. With the hires of Joana Nash and Ron Guido as experienced senior quant portfolio managers, Realindex has also beefed up its quant research capabilities.

The team is nimbler now for prioritization and effective collaboration on research initiatives and efficient implementation of the research outcomes, although it is preferred to have clearer lines between the research and portfolio management teams. The visible progress made in the trailing 18 months in research projects (for example, ESG factor impact on price and incorporating intangibles into the book value) augmenting the investment process through the implementation of novel signals is testimony of the team’s collective ability. The recent departure of experienced senior portfolio manager Raelene De Souza is unfortunate. Historically, Realindex has been successful in attracting top investment talent. But the length of their association with the firm has been shorter than it is prefered.

Performance

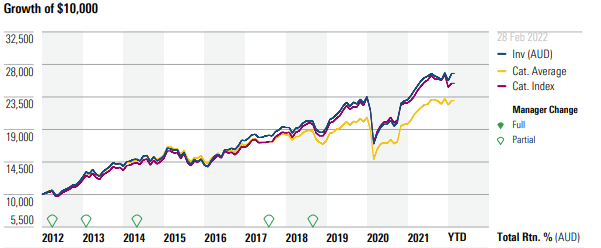

Realindex Australian Shares has delivered impressive peer-relative performance from inception through February 2022. Its five-year return of 8.5% per year as of February 2022 has easily outpaced the category average but only matched the broader market’s index return, indicating the tough environment it has been for value managers. This performance is principally attributed to the overweighting in materials, underweighting in healthcare, and energy. Better stock inclusion from the resources and consumer cyclical sectors has been additive too. Specifically, overweightings in BHP Group and Wesfarmers has added to performance and offset marginally by the overweighting in Westpac Banking. Amid the pandemic-induced uncertainties across the market, the strategy was admirably more resilient than the average category manager. The impressive outperformance was largely fueled by the strategy’s overweighting in materials, consumer cyclical, and consumer staples (a recurring theme across short- and long-term performance), although slightly offset by its overweighting in financial services. Over the trailing year through February 2022, the strategy has outperformed the S&P/ASX 200 Index but marginally stayed below the category average as value stocks have staged a reversal.

About Fund:

Realindex forms a universe of Australian companies based on accounting measures.Factors such as quality, near – term value and momentum are applied to form a final portfolio of companies. The resulting portfolio has a value tilt relative to the benchmark and provides the benefits of being lower in cost, lower turnover and highly diversified compared to traditional active investment strategies. Realindex overhauled its investment team with an aim to create a nimbler team structure and has hired investment professionals with a high skillset and experience level. The new team has made real progress in the trailing 18 months defining the research agenda and prioritizing projects in terms of their potential to value add. These developments paint a positive picture for the strategy; however, investors should note that the team’s tenure is short and Realindex’s track record in team turnover has not been impressive. As such, it is alleged for the investment team to exhibit longevity before experts’ conviction level is strengthened.

(Source: Morningstar)

General Advice Warning

Any advice/ information provided is general in nature only and does not take into account the personal financial situation, objectives or needs of any particular person.

Approach

This strategy aims to track the Bloomberg Ausbond Composite 0+ Index with a tracking error of 0.05% per year or less (before fees). IShares is typically able to achieve full replication of the government-bond component in the portfolio because of ample liquidity and breadth. To alleviate liquidity challenges, the firm uses stratified sampling to acquire corporate and supranational exposures–an industry-standard approach, but one in which iShares excels thanks to its sophisticated global trading systems and experienced team. When the team can’t buy all the bonds in the index at a reasonable price, it will instead buy a basket of bonds that has similar credit and duration risks within allowable tolerance ranges. The team also employs strategies like securities lending to generate additional returns, helping to offset the performance drag from factors like fees and trading costs. IShares’ scale further minimises trading costs; a large active book and the firm’s ETF business allow for cross-trades and wide broker access. IShares thus executes trades cheaply, which is crucial in index fund management. It’s worth noting that Bloomberg’s index assumes distributions earn no interest, whereas iShares may accrue interest on its distribution cash balances. This may cause some tracking error, but ultimately it is a positive tailwind.

Portfolio

This strategy aims to fully replicate the Bloomberg AusBond Composite 0+ Index. Factoring cost, liquidity, and existing diversification if it doesn’t make sense to own all the bonds on issue, it will use stratified sampling to buy a basket of bonds with similar credit and duration risks. As of 28 Feb 2022, the index was composed of government and semigovernment bonds (85%), supranationals (5%), and corporate bonds (9%). The fund invests in high-quality bonds, with AAA rated debt constituting 71% of the benchmark’s quality exposure. Banks and other financials issue most of the credit in the index. The fund’s duration continues to increase with the benchmark as yields mostly hovered around historic lows barring the recent spike, up from 4.95 years at October 2016 to 5.8 years at 28 Feb 2022. The lengthening duration is a result of Commonwealth Government Bonds being issued at longer tenures, such as 30 years. But it means the fund faces the risk of rising yields globally, when we would expect active managers in this space to outperform their long-duration passive peers. Overall credit quality and appropriate diversification make this strategy an appropriate core exposure.

Performance: In terms of Annualised and Cumulative basis

Top 10 Holdings of the fund

About the fund

The fund aims to provide investors with the performance of the Bloomberg Aus Bond Composite 0+ Yr Index SM, before fees and expenses. The index is designed to measure the performance of the Australian bond market and includes investment grade fixed income securities issued by the Australian Treasury, Australian semi-government entities, supranational and sovereign entities and corporate entities.

(Source: Morningstar)

General Advice Warning

Any advice/ information provided is general in nature only and does not take into account the personal financial situation, objectives or needs of any particular person.